Don't Short Science Projects

I forecast the SpaceX IPO and propose a Nasdaq ex-Musk ETF, but I'm still bullish on Big Tech because profits and earnings matter, and they're still chock full of both.

Welcome to this week’s edition of The Macro Obsession.

The best round-up of current events and trends in finance, tech, and the real economy currently in your inbox!

Issue #47—Week of May 25th, 2026

Forced Buyers Wanted

Building the Machine God

Computing for Profit

The Nasdaq Will Survive

Forced Buyers Wanted

Financial news had been rightfully dominated by the news of the SpaceX (SPCX 0.00%↑) IPO, now slated for mid-June. And to top it off, they got approval to enter the Nasdaq 100 after 15 trading days (ETF Stream).

The S&P committee is considering changing their criteria to allow unprofitable firms into the S&P 500. They are setting up SpaceX to get inclusion straight into both indexes, ensuring forced buying from passive funds basically out of the gate. I expect this to be regrettable.

A quick note on timing before we go any further. Don’t look at days 1-200. They will likely be great thanks to all the forced buying from the indexes; it’s almost mechanically destined to be a good few months so long as the broader market holds up. To fuel the index buying and get to the free-float requirements the indexes have for accelerated inclusion, insiders are being given express permission to sell earlier than the previously given timeline (Quartz).

The fire will need fuel. Pre-IPO investors are eager to provide.

The setup is there for a great IPO and follow-through for the period in which everyone will be watching and judging it, likely fitting the average tech IPO pattern.

So for the savvy trader, this may be an opportunity to catch a ride alongside the funny market mechanics. Short-term investors could be bullish here basically regardless of what the financials say. But be warned, the company underneath is hideous from what we’ve seen so far. And I mean hideous.

The breakdown of the S-1 filing has already been done better than I can, so I will leave it to the great Patrick Boyle for those who want the full view of all SpaceX’s red flags; it looks like Tiananmen Square.

Building the Machine God

I was initially excited at the rumors of SpaceX going public in the past years because I knew that the Starlink business is excellent.

Satellite internet is a profitable business, and Starlink took it to a new level. Its first-mover advantage is structural because of their optimal placement in orbit, and nobody else can take that from them since they already occupy it.

The other half of the business, which Starlink is basically subsidizing, is designed to replace NASA.1 The self-landing rocket tech was a genuine innovation in space logistics, and it seemed like Starlink could keep the ramp going until the government contracts became profitable.

On paper, it was an actually compelling space company, I thought, and of course valuations would be nuts because Musk is involved. It was early innings but had a lot of promise.

Then they merged with xAI, Musk’s AI company that had previously merged with Twitter. So suddenly, SpaceX had three pits of quicksand all fighting for Starlink dollars.

Regular readers will know that I am very bearish on frontier AI labs.2 The phrase I’ve been using is that I believe we are living through the largest willful act of capital destruction of all time. When it’s all said and done, I expect these frontier labs (OpenAI, Anthropic, xAI, etc.) to be worth more dead than alive.

The S-1 filing confirmed that SpaceX is going full AI. It didn’t buy xAI as a side project or to leverage Grok. It bought xAI to become an AI company.

Here is the SpaceX mission statement directly from the document itself (SEC):

Our mission is to build the systems and technologies necessary to make life multiplanetary, to understand the true nature of the universe, and to extend the light of consciousness to the stars. To do this, we have formed the most ambitious, vertically integrated innovation engine on (and off) Earth with unmatched capabilities to rapidly manufacture and launch space-based communications that connect the world, to harness the Sun to power a truth-seeking artificial intelligence that advances scientific discovery, and ultimately to build a base on the Moon and cities on other planets.

You read that right. SpaceX is going to build the machine god. This line is one for the textbooks. Let me isolate it for us here:

…to harness the Sun to power a truth-seeking artificial intelligence…

Apparently, this will be done via launching solar-powered data center satellites into space. I am skeptical, but intelligent people tell me that I am wrong. Take a look at the thread here with Mulberry Investment Research and make up your own mind/chime in.

Computing for Profit

It’s a good thing for Mr. Musk that this machine god is projected to be hella profitable. I mean, they’re not currently profitable; they lose ~$4B/quarter. But once they build it all, it’ll really kick in, they swear.

They expect that Grok will make up 80% of their total business once it’s all said and done. That’s what “enterprise applications” are: the renting out of AI. Its addressable market is the size of the EU’s GDP. No big deal.

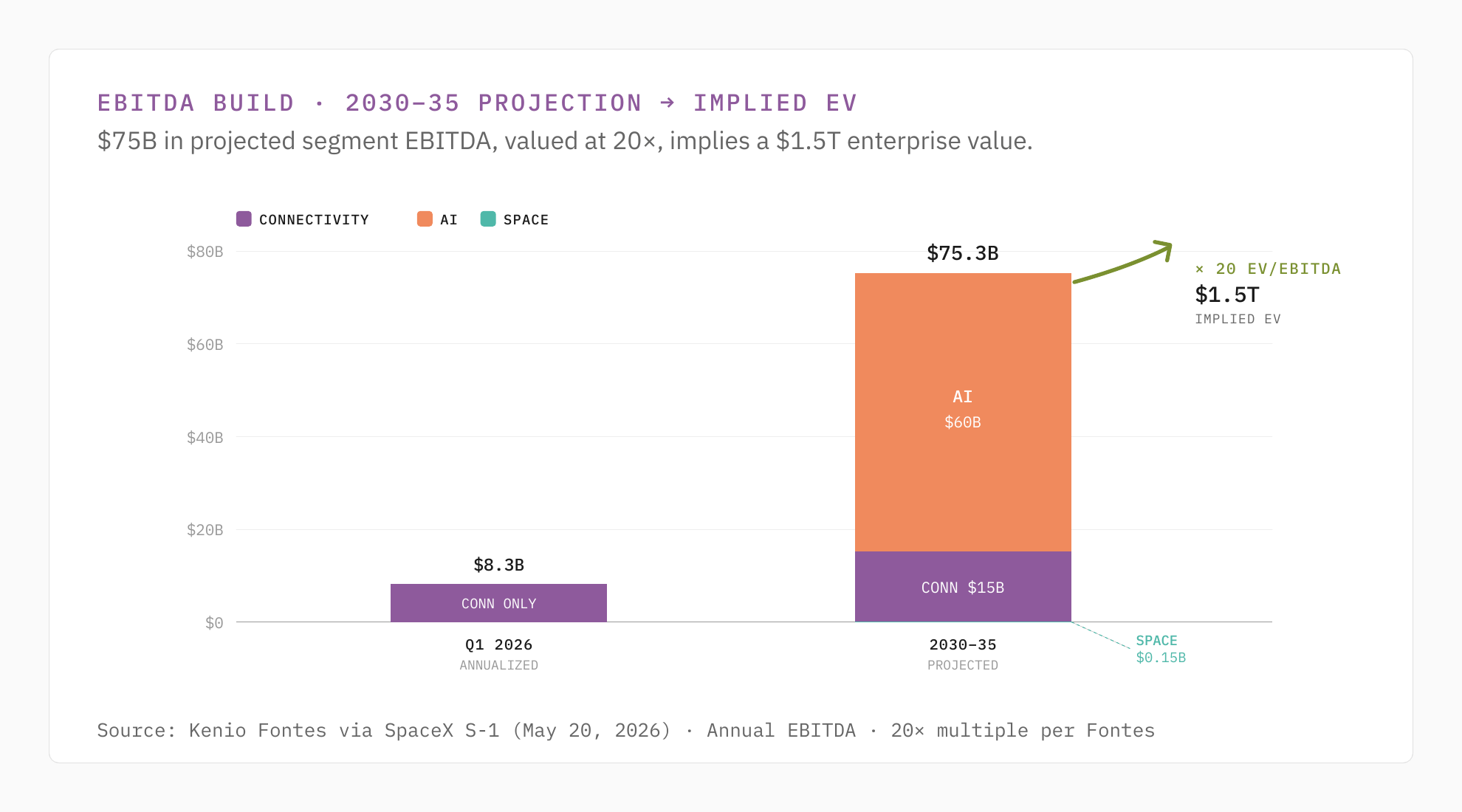

My friend and colleague Kenio Fontes over at Seeking Alpha [GIFT LINK] tried to put a figure on the long-term outlook given the current numbers and some assumptions. Here’s a fundamental investor’s take:

Although being very intangible, I tried to estimate some numbers for SpaceX. In AI infrastructure, if…between 2030 to 2035…[SpaceX] manages to deliver…80 GW and a revenue of $3 billion per GW (normalizing)...

For Connectivity and Space, I was more conservative. Something close to ~27 million Starlink subscribers, which basically means maintaining the current growth pace…For Space, since it matters very little in the final valuation, I only considered a mid single digits growth...

…in this scenario, we have a proxy of SpaceX’s adj. EBITDA, something close to ~$75 billion for 2030...20x = $1.5 trillion [enterprise value]. This already tells me that [a $2 trillion IPO] would not be very interesting, but $1.5 trillion is “decent.”

So come June 12th or whenever the IPO ends up being, that’s what to look out for. But keep in mind that this assumes SpaceX is right about their projections. And they’re projecting that in 5 years, Grok will be 91% of their earnings growth.

Given how suspicious I am of the current AI demand figures that we are using for projections—see “Distilled in Menlo Park” (TMO #41) where I discuss how the reason AI revenue is still rising can be attributed to bad actors, among which are hyperscalers like Meta (META 0.00%↑)—it does not look good for SpaceX that they are basically saying, “We think the rest of our business will just be in service to the machine god.”

The best part of the current business, Starlink, is listed as one of the worst parts of the future business in their vision. That tells me a lot about the ambitions, although so does Musk’s compensation package being partially contingent on a Mars colony population milestone. I’m not kidding. He really needs to get 1,000,000 people on Mars or he can’t unlock all of his vested SpaceX shares.3

Just do me a favor and don’t short this thing. The mechanics of its listing and index inclusion are very strong and don’t give a definitive timeline. And it’s always good to adhere to the old trader aphorism about unproven businesses:

Don’t bet against science projects.

But I won’t be betting on it either, at least not directly.4

I’ve been wondering if there will be an opportunity for an ETF that is the Nasdaq 100 or S&P 500 ex-Musk or excluding TSLA and SPCX. I bet that ETF could charge 75 bp!

After workshopping tickers with my lovely wife, I settled on $XMSK.

Don’t worry, she’ll get royalties if it goes to market.

More Below, But ICYMI

The Nasdaq Will Survive

Now that we’ve gotten through my bearish assessment of SpaceX, let’s talk about why I’m still pretty full-steam ahead on the rest of the market, apart from last week’s tirade on profitability, “The P in S&P Stands for Profits” (TMO #46).

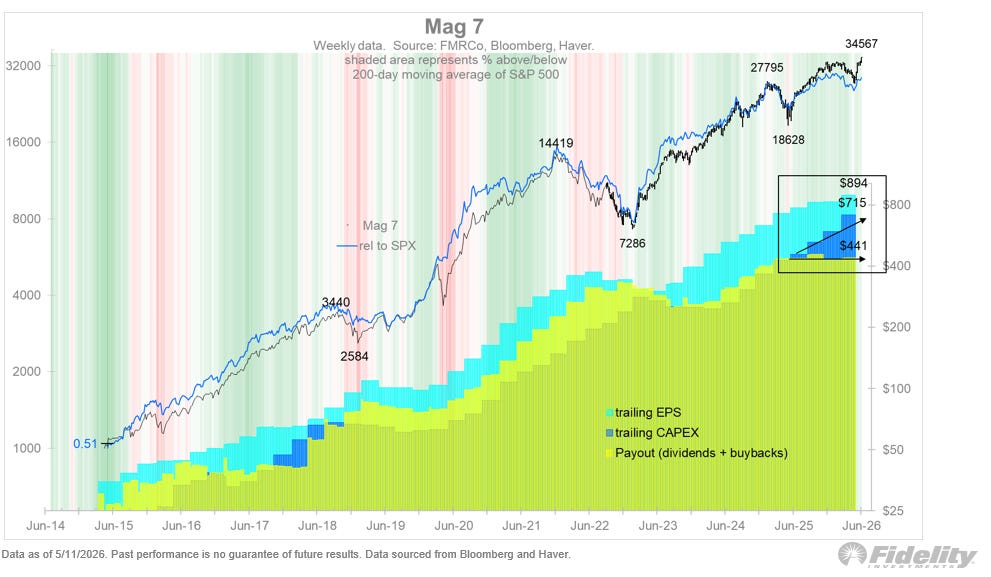

The first is that the Mag 7 have been able to keep up their earnings even while they blow up their capital expenditures (CapEx) on AI. I understand the argument that it takes money to make money, and I’m not worried about their spending on infrastructure per se.

I just want to make sure it makes sense, and so far, it seems to, as earnings trends are holding up even if dividends and buybacks have been flat YoY.5

I would rather not be out here trying to brush off the fact that we’re covering the planet in data centers just as fast as we were trying to cover it in solar panels 4 years ago, but profits justify price, and that’s just how markets work (TMO #39).

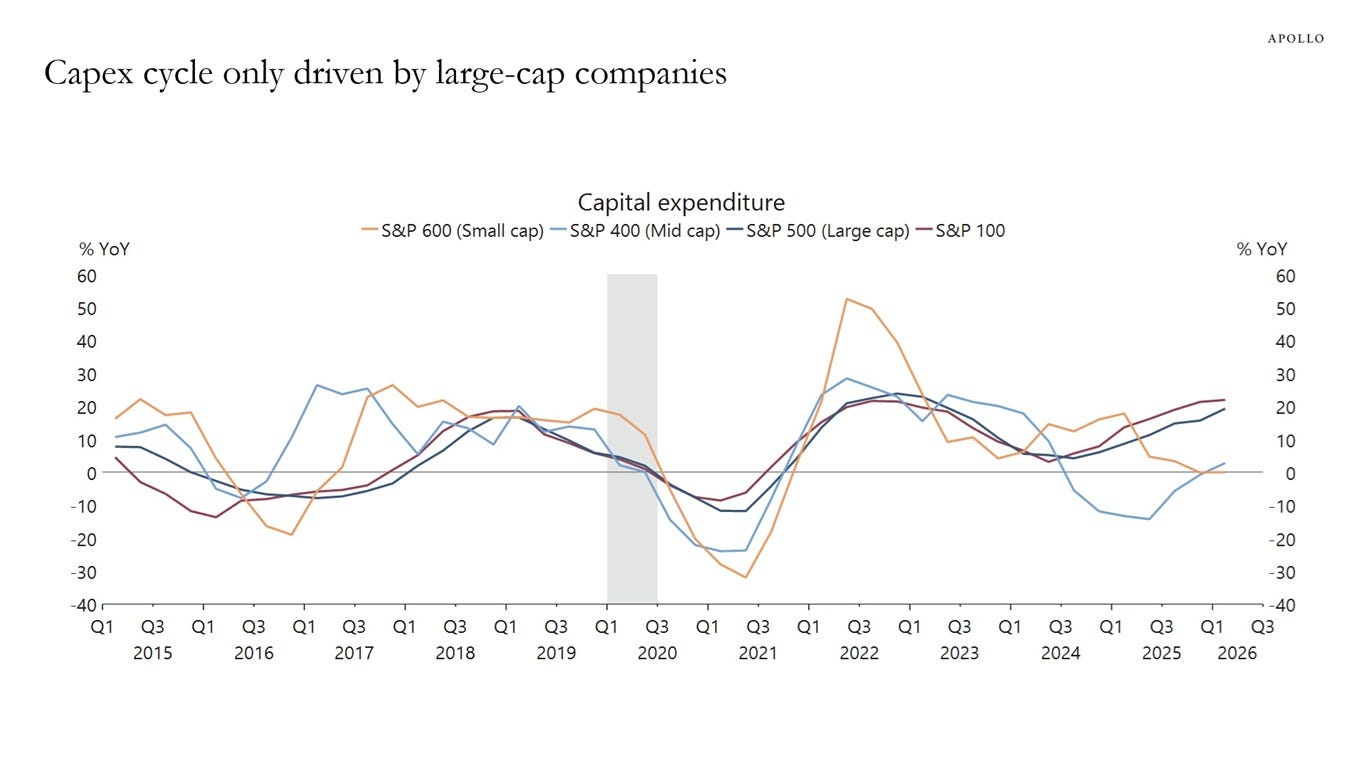

But not everyone is doing tons of CapEx. It’s really just the big firms. They can take some time off buybacks to build things without breaking the market. The rest of the economy, which employs the majority of people, isn’t blowing all their cash on CapEx. That’s reassuring, actually.

If this newsletter made you think of a pal, send it to them and tell them why.

See you next week.

I am on the fence over if this is a good thing or not. I am leaning toward not.

I see their utility and I use their products, but I do not believe that they will be able to be profitable selling compute as a service given how deeply subsidized it must be. Estimates I’ve seen put the spend at $10 for every $1 of consumer cash coming in.

For the record, none of that matters because he gets to vote with all the shares, even if he can’t unlock them. He doesn’t really want to unlock them because he doesn’t want to sell them. He ultimately just wants to pass all of these shares to his children. That will happen whether he builds a Mars colony or not.

Since I have passive index exposure, I may have no choice.

I’m assuming that the phantom demand that I believe is plaguing the numbers of frontier labs is not a real factor here. This is all mostly software and ad revenue.

Wow, this a doozy Jack. Solar-powered data center satellites is a mouth full but makes a ton of sense in theory. Of course, I'm no engineer so good luck fellas!! And $XMSK is hilarious! I'm pealing 5% out of oil and it's going to either UFO or MARS. Leaning UFO because of size but maybe this is a time where being in a smaller fund is almost sure to be of greater benefit. What do you think?