Credit Doomers Are Losing

I dismiss fears about debt, the S&P is a profit machine, we get some data on commuters, and a few AI charts make their way in at the end.

Welcome to this week’s edition of The Macro Obsession.

The best round-up of current events and trends in finance, tech, and the real economy currently in your inbox!

Issue #46—Week of May 18th, 2026

Everything’s Coming Up Credit!

The P in S&P Stands for Profit

Commuting Straight Outta Hell

AI Chart Potpourri

Hey folks!

This week, I published my monthly series where I go over all the ETF launches from the previous month and give my thoughts on them. It’s a great way for folks with not a lot of time to keep up with new fund launches.

Due to its popularity, I will be moving it to its own mailing list for next month. It will live in its own section in TMO. Don’t worry, you won’t have to do anything!

But ICYMI from earlier this week:

The ETF Obsession | April 2026

It's a little late, but I reviewed all the ETF launches in April! Of 93, there were 49 even worth looking at, and only 10 of those got a positive rating.

Now, on to the newsletter!

Everything’s Coming Up Credit!

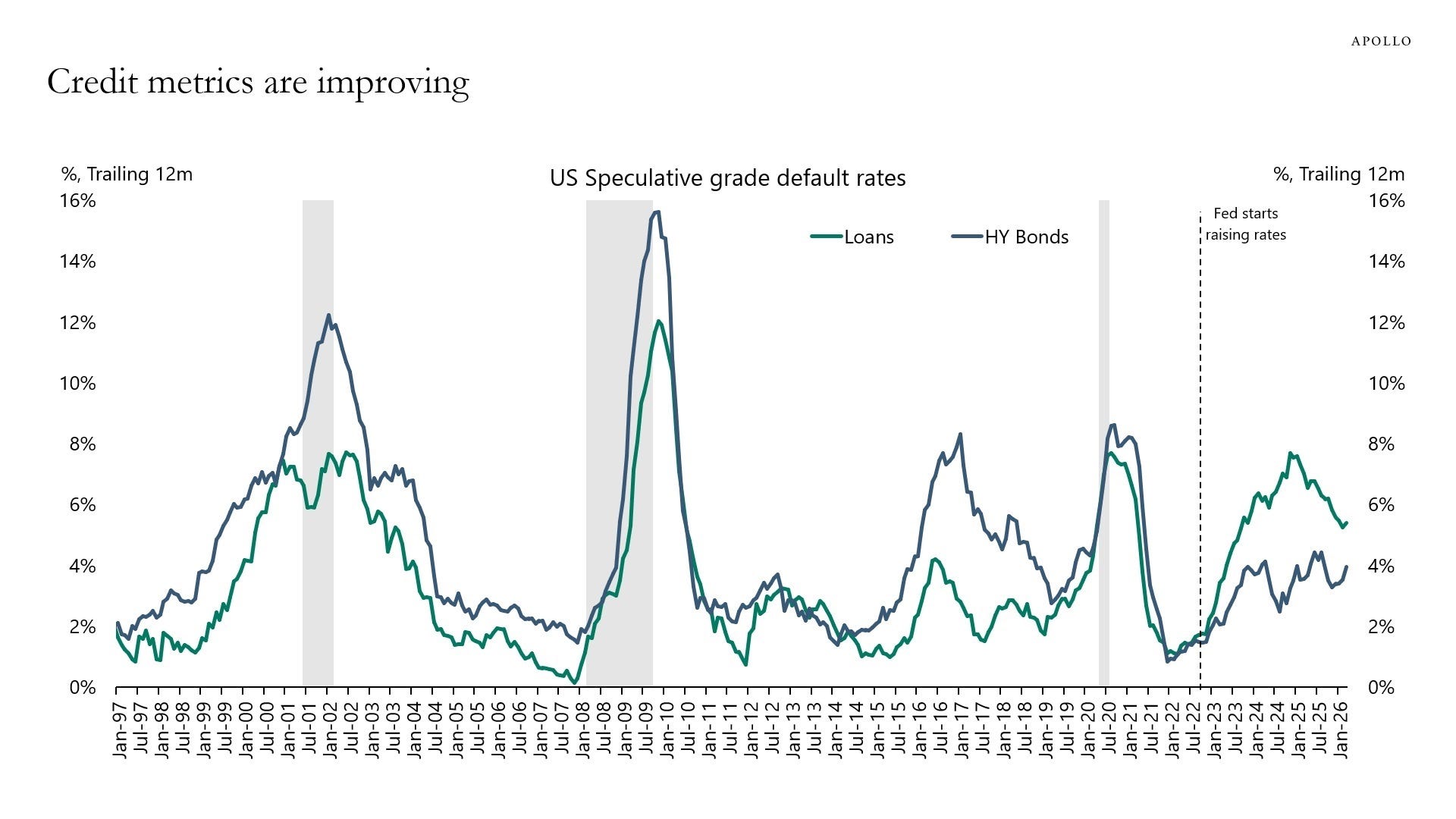

I haven’t brought up our old pal credit in a couple of weeks, not since I evoked private credit in “VC Has a Knife to PE” (TMO #42) about a month ago and discussed how it’s not been doing so well. Cue Apollo (APO 0.00%↑), who of course has a mighty steed in this race, putting out charts trying to convince us of the opposite for credit conditions.

I will say, they are compelling charts. There’s a few of them, all published over the last two weeks-ish. I won’t call it a coordinated effort, but I do see Apollo talking its own book here.

The data is real, though, and it’s bullish for the economy as a whole even if the pain is still structurally higher than it was pre-2022. It’s coming down, not continuing to rise, despite the popular narrative.

That’s important to recognize, because the zeitgeist is going to keep telling us it’s getting worse all the way down to the bottom, through the trough, and most of the way back up.

But take a look—junk loan defaults are coming down, having peaked last year, although junk bonds are still grinding up slowly. Even these are below their near-term peak.

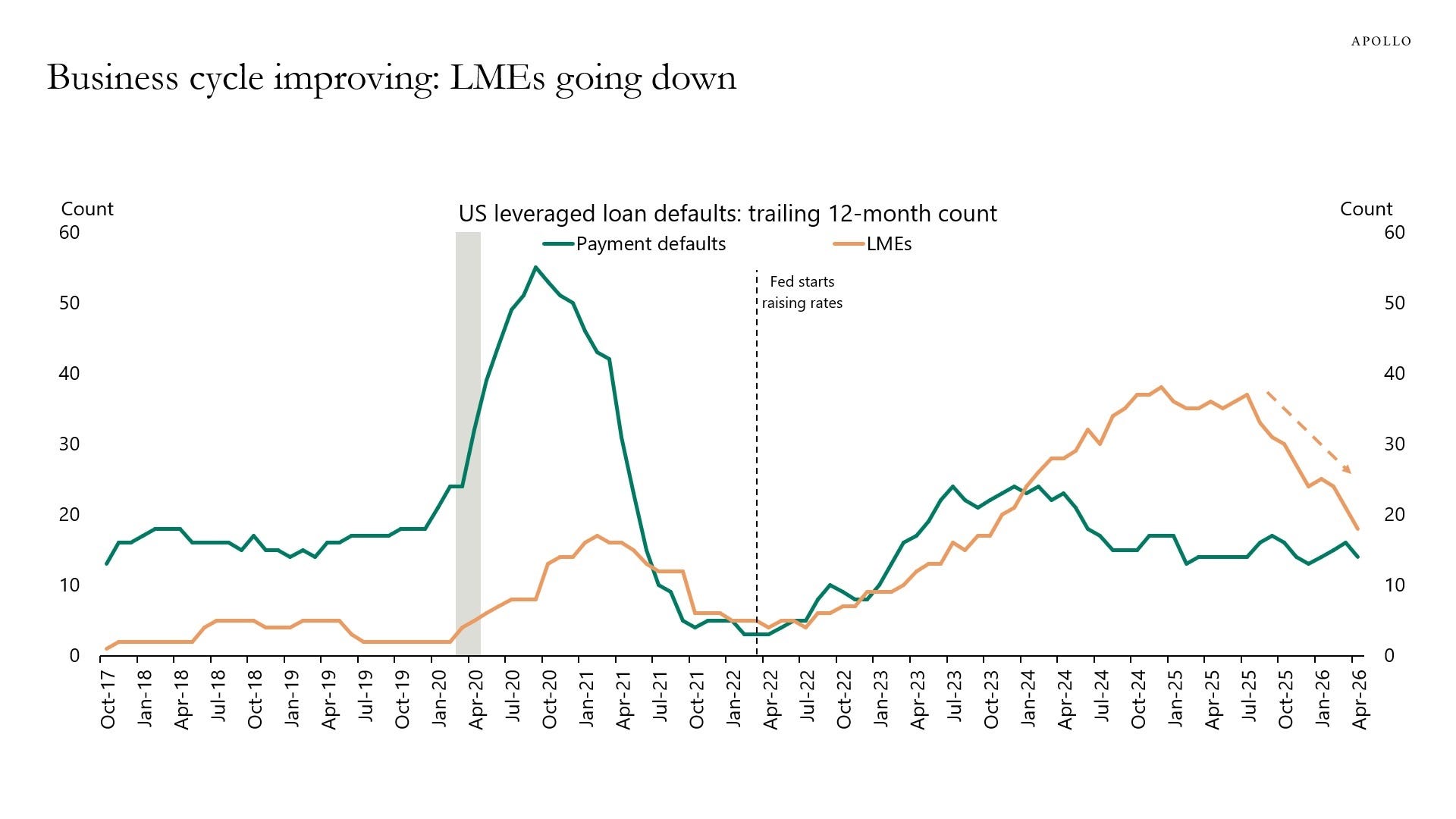

Leveraged loan defaults are elevated but not rising, and the LME1 rate is falling quickly. That’s a very positive sign.

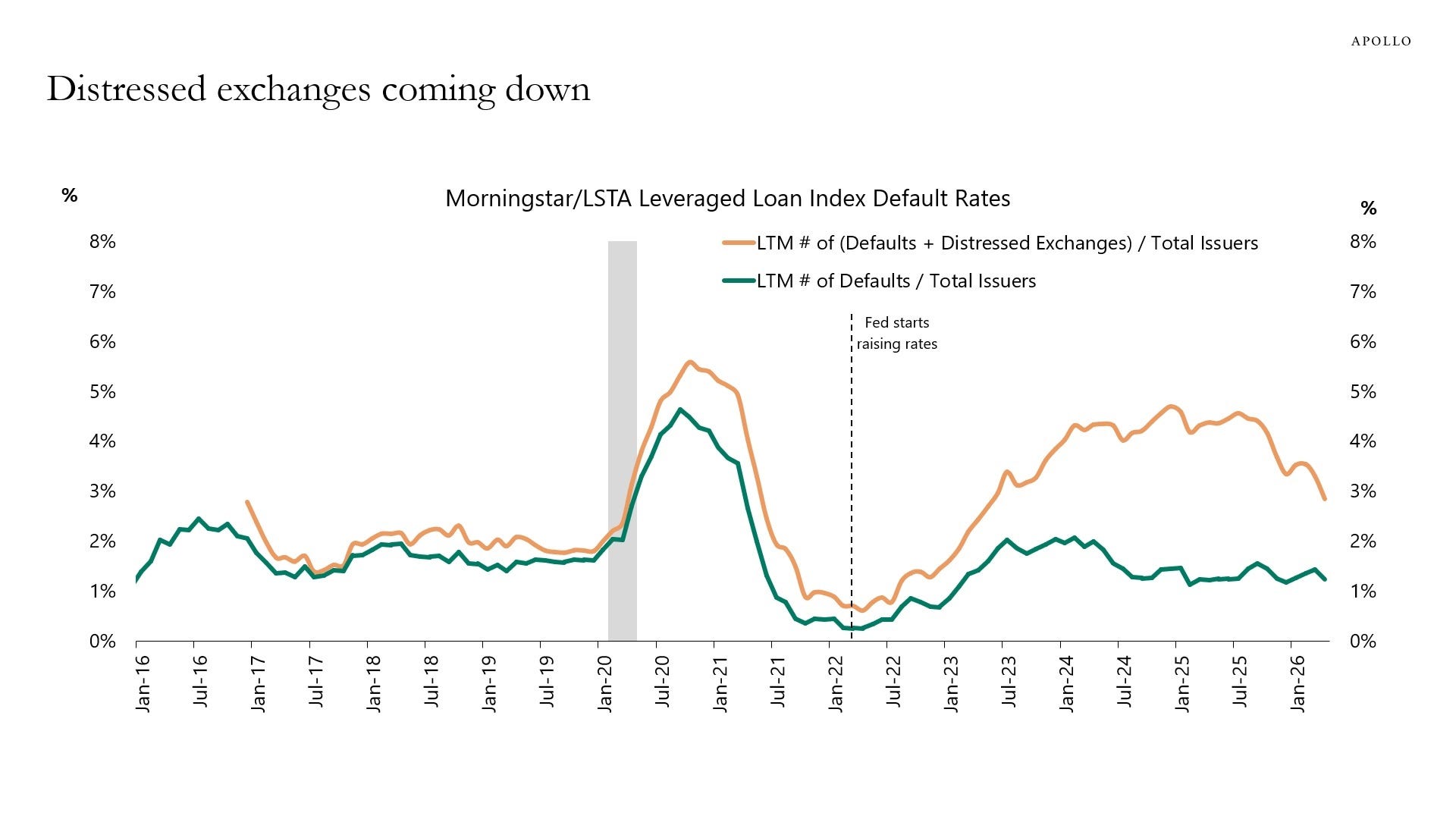

The leveraged loan index is doing well on the whole, with distress coming up far less often than at the peak; we’re back at 2023 levels now.

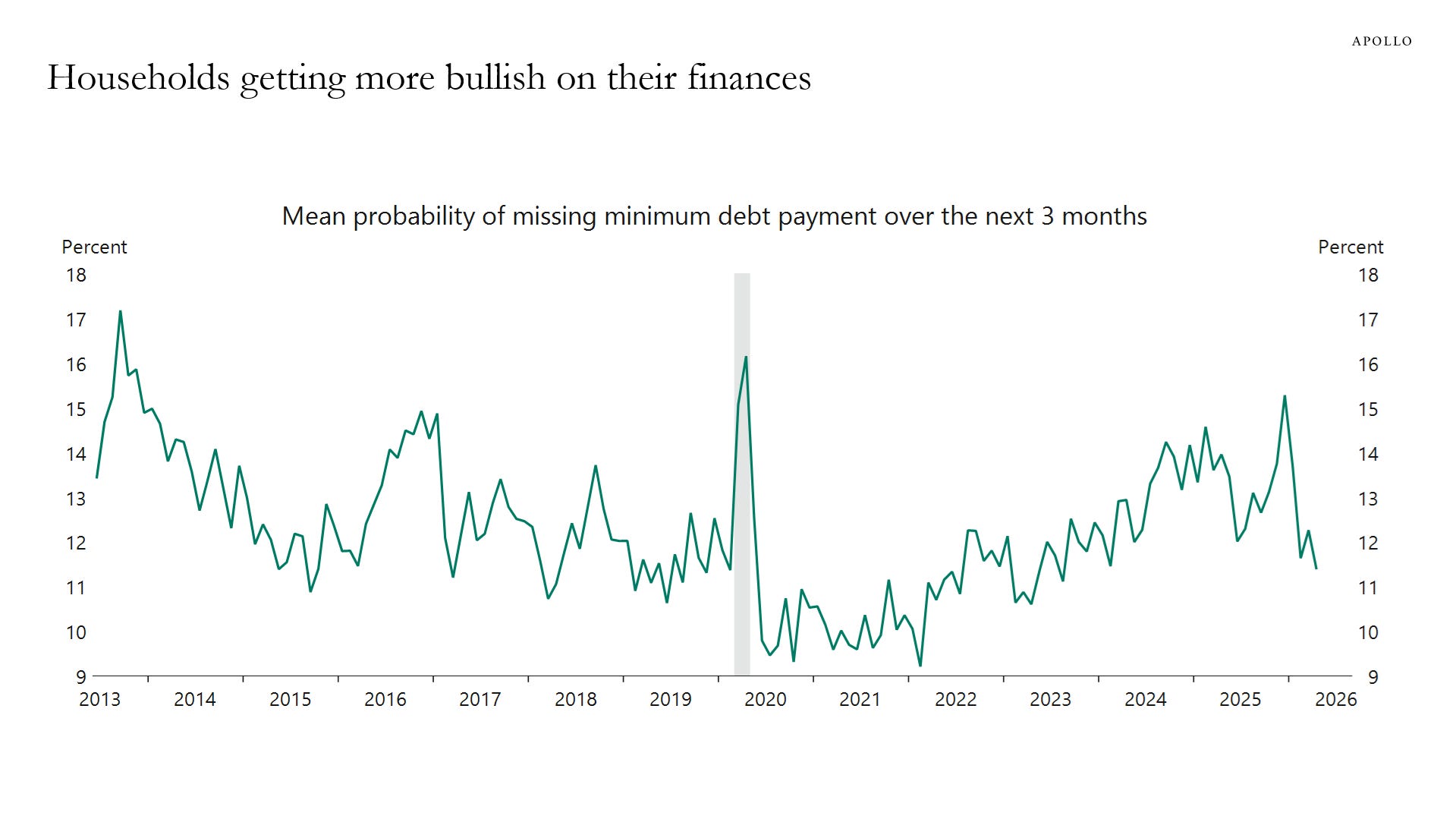

Even households are doing better, with their stress falling this year as well, although gas prices will halt the progress this month. Regardless, being at a level lower than any time in the past two years is solid progress.

This is what having “taken our rate medicine” post-ZIRP looks like, apparently. The question is how fast we mess it up. Given the current oil situation, we’re already on the way there.

The P in S&P Stands for Profit

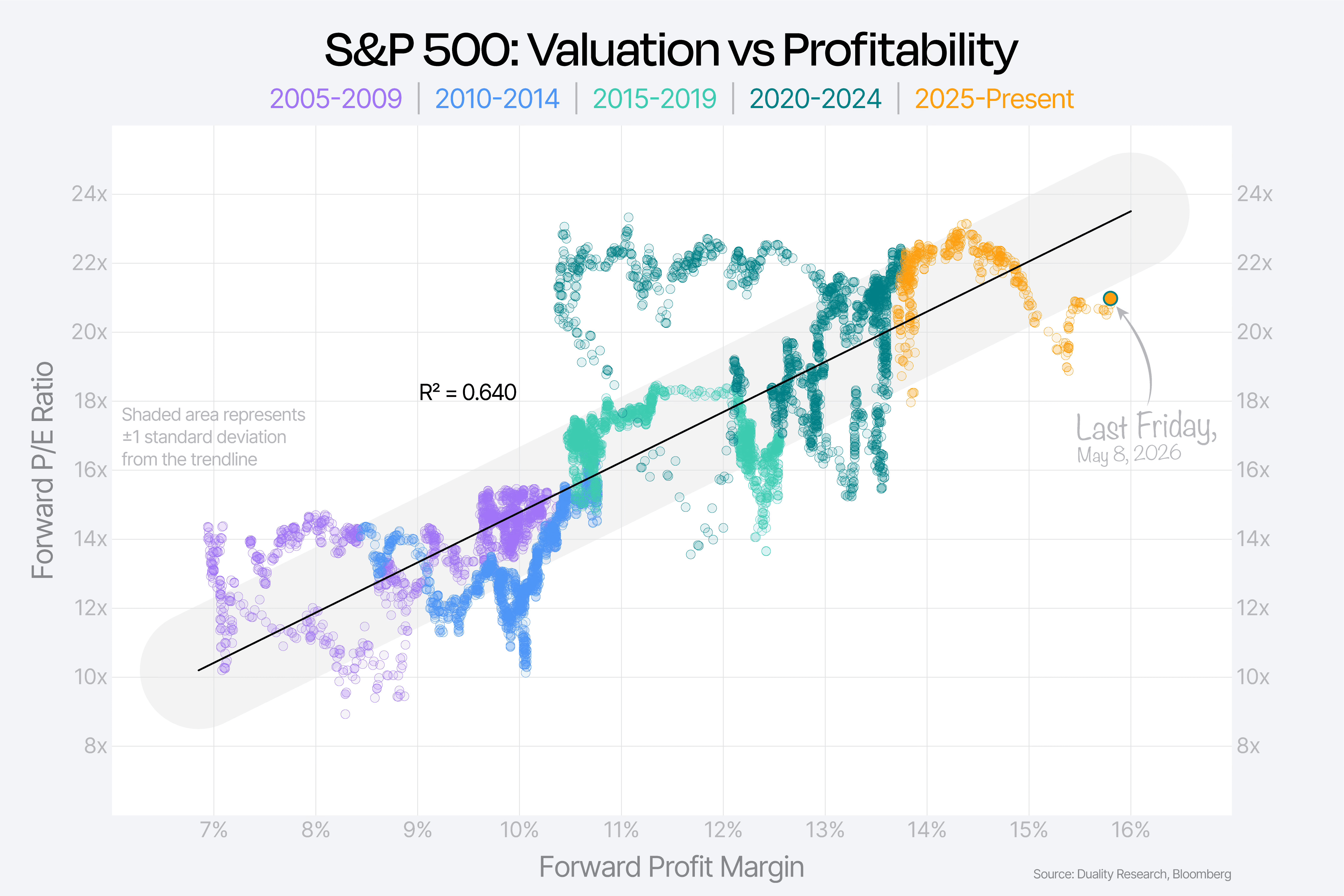

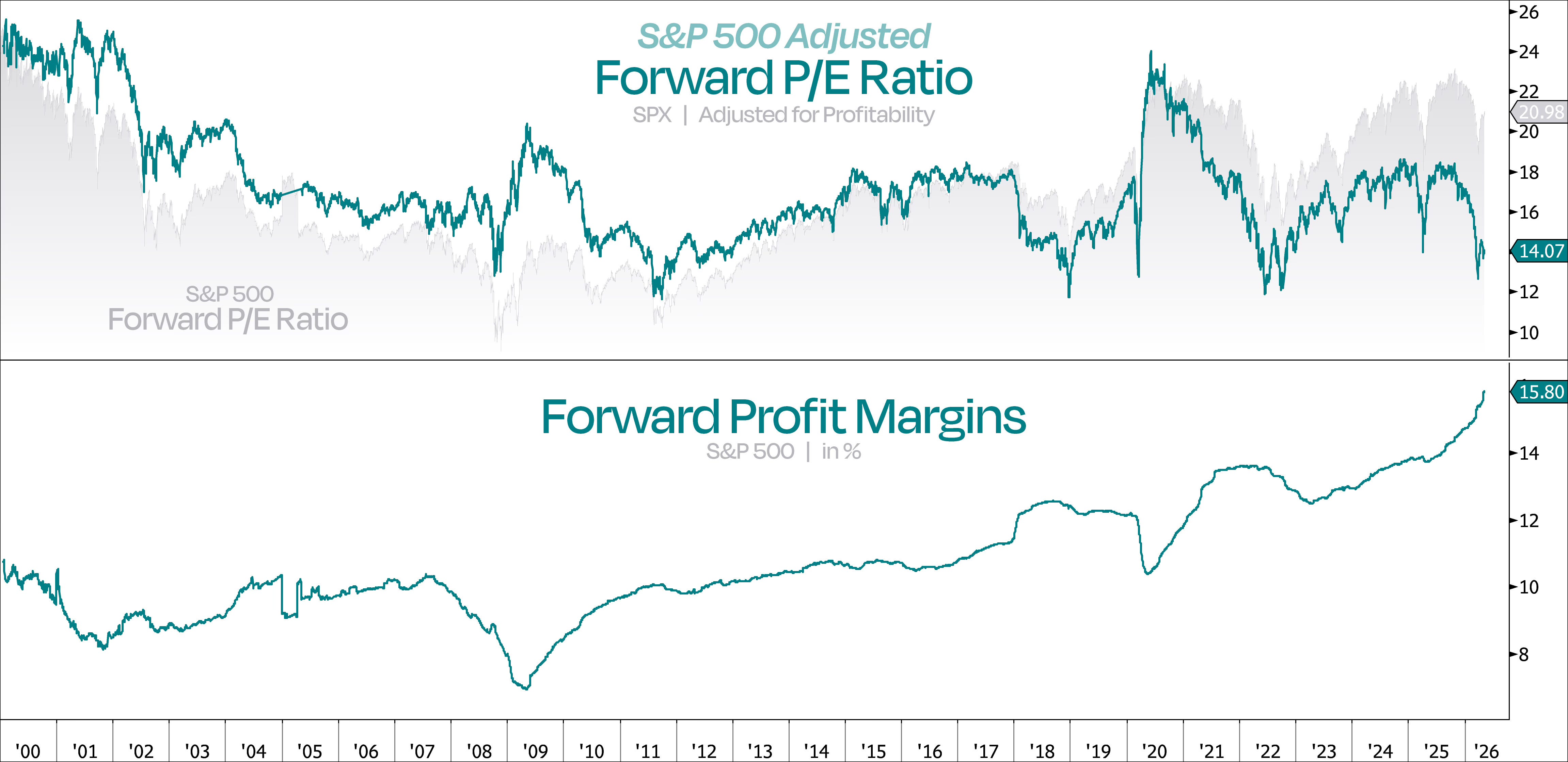

Regular TMO readers will know that the thing that keeps me bullish on markets is profitability. If you haven’t seen the most obvious piece of evidence for this—a beautiful chart produced by the folks over at Duality Research—take a gander.

This is the S&P 500’s valuation adjusted for forward profit margins, week by week, for the last two decades. As profitability has increased, so has the average PE ratio. I evoked this chart, and how low we’d gotten on it, back in “Calling the Bottom” (TMO #38), but here’s the update. We’re still below trend.

Here’s the profit-adjusted PE itself, which is just so—say it with me—buyable. Historically, buying at 14x has been a smart move.

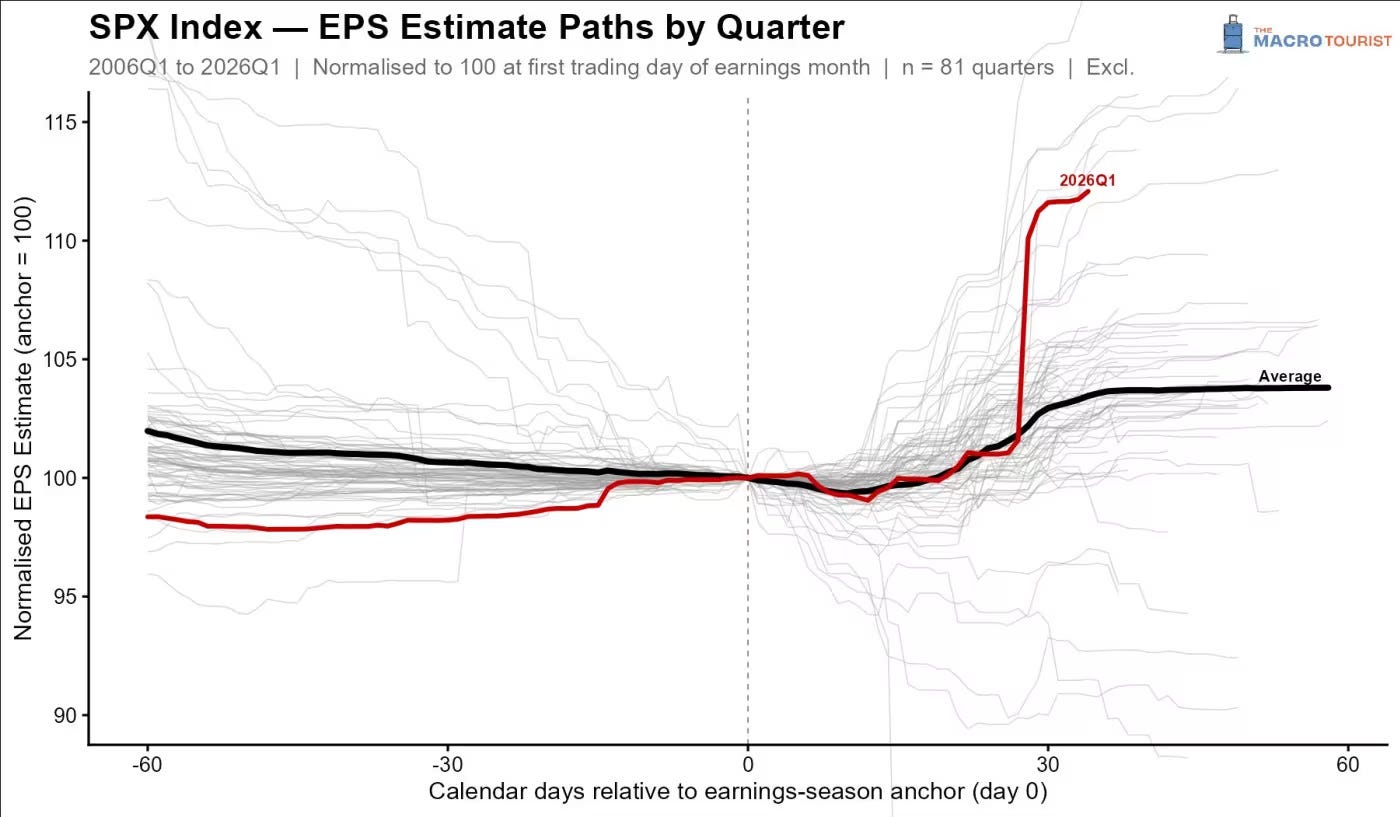

S&P 500 earnings really are out of control, to be fair. The jump up in Q1 was very aggressive and really explains why the market has been ignoring most of the geopolitical stress that is still ongoing in the Middle East.

For now, this has me more bullish than anything else, and I’m just trying not to think about how priced in oil sticking >$80 for a year or more is.2

The S&P 500 is earning investment in real time; there is little reason to eschew a market that makes this much and is priced that low (from a profit-adjusted figure). The fogey Shiller PE folks will come at me for this, but the S&P is just buyable right now, hands down.

I keep banging the desk over this because the pricing isn’t exorbitant and driven by multiple expansions. It’s backed by earnings and profit margins.

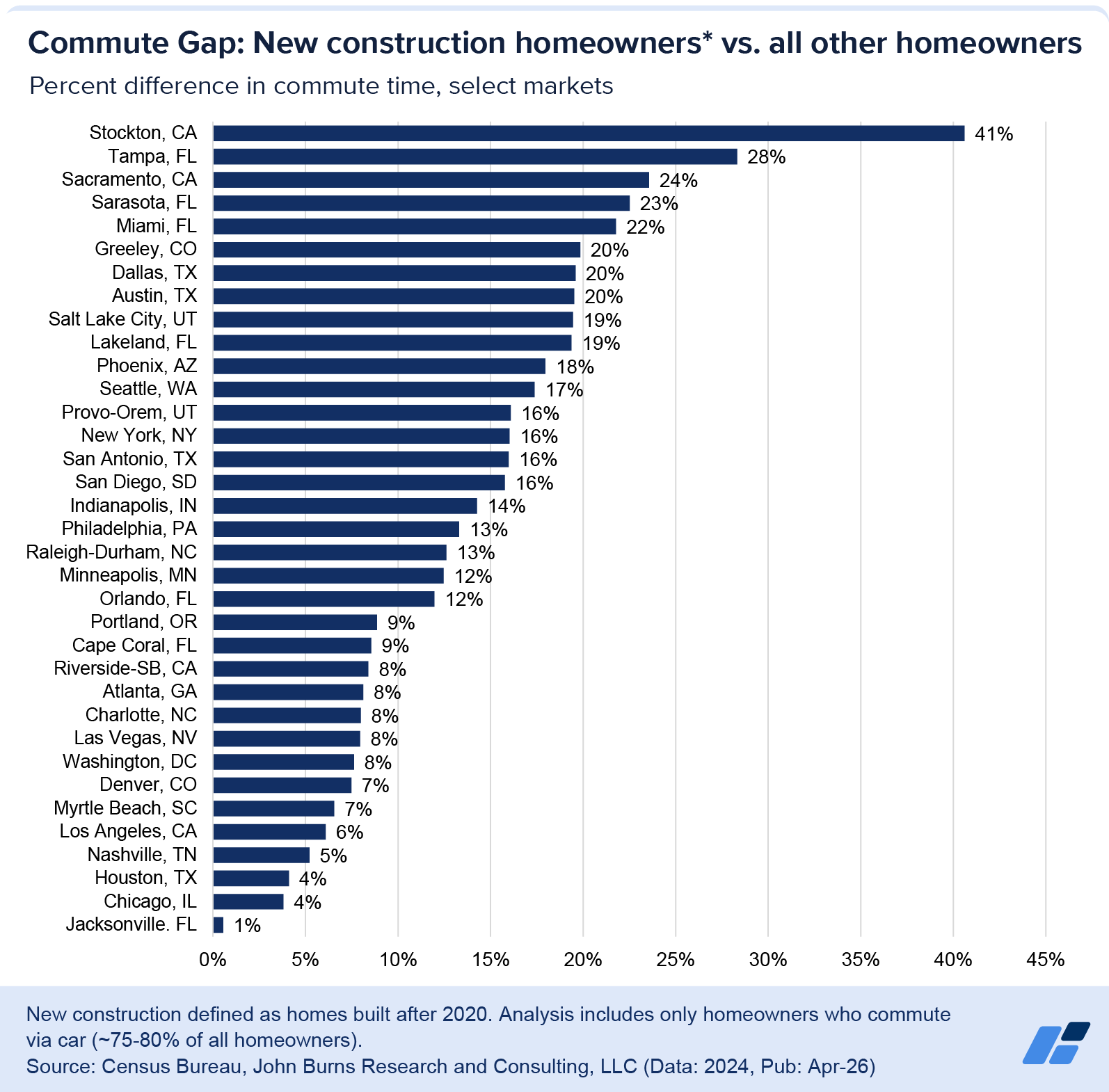

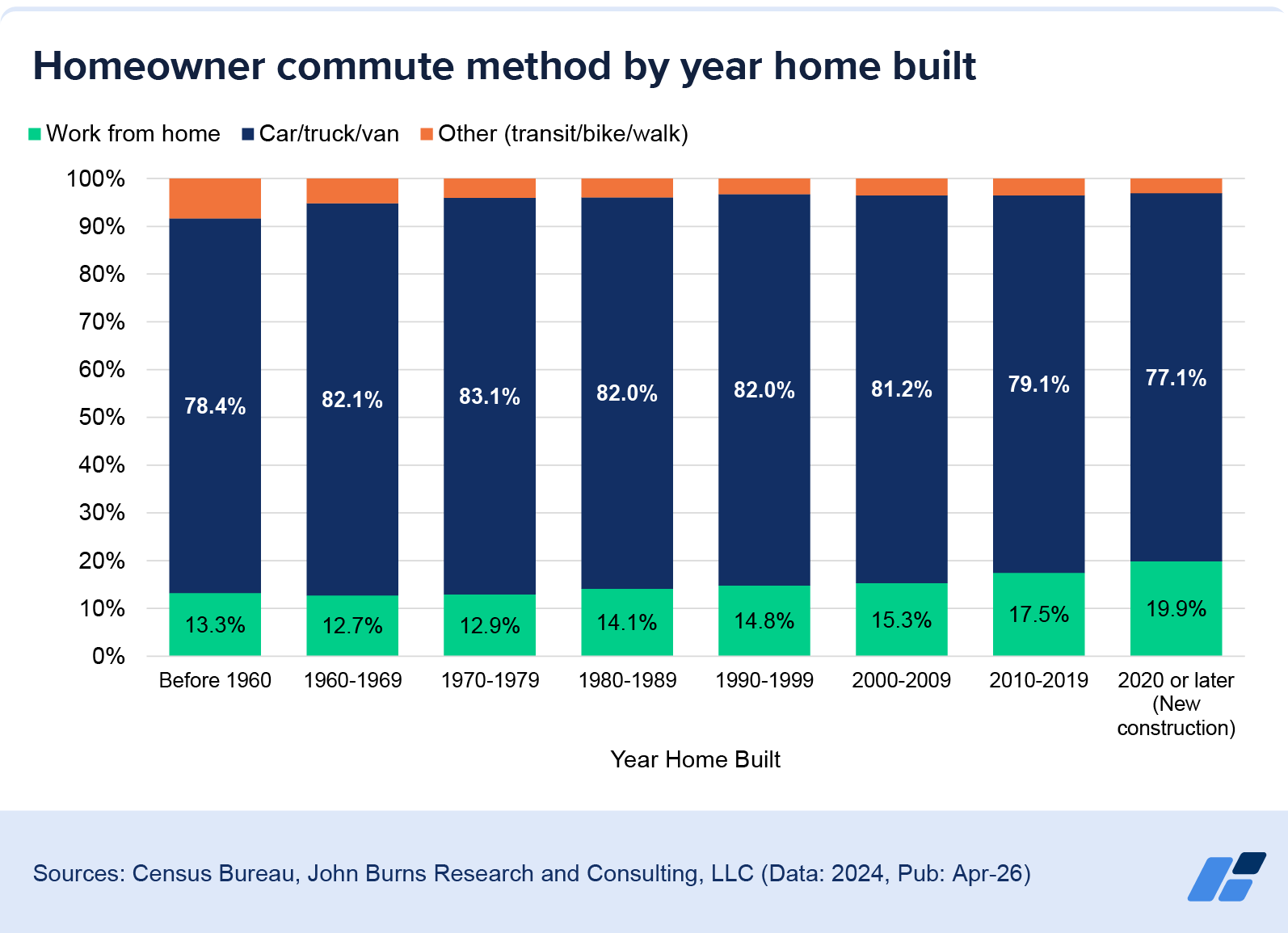

Commuting Straight Outta Hell

I saw a few interesting charts about commuters this week, which made me think that it would be fun to follow up on “Return to Office Returns to Sender” (TMO #42).

This was the first animated chart that’s hit my desk in a while. It’s showing how new home constructions are increasingly being built deep into the suburban sprawl, away from jobs. Over time, this has only gotten worse, and new constructions now average 1 hr/day commutes.

This makes sense, since homes from the 1960s and newer are likely still fine today if they were kept up on.3 So newer homes needed to be built on unused land, which meant that they ended up further and further away from economic hubs and thus had longer commutes.

It’s regional, and it really varies by city, not state. Jacksonville has very egalitarian new construction vs. existing home commute times, but Tampa and Miami (both in-state but far away) make the top 5 worst cities for new construction owners.

But despite all the hassle, this has not driven much public transit adoption. Work from home rates go up the newer your home is, although I suspect that the big jumps up are from relocators who moved from a high-income area to a low-income area and arbitraged the low rates and pandemic-era work from home policies.

More Below, But ICYMI

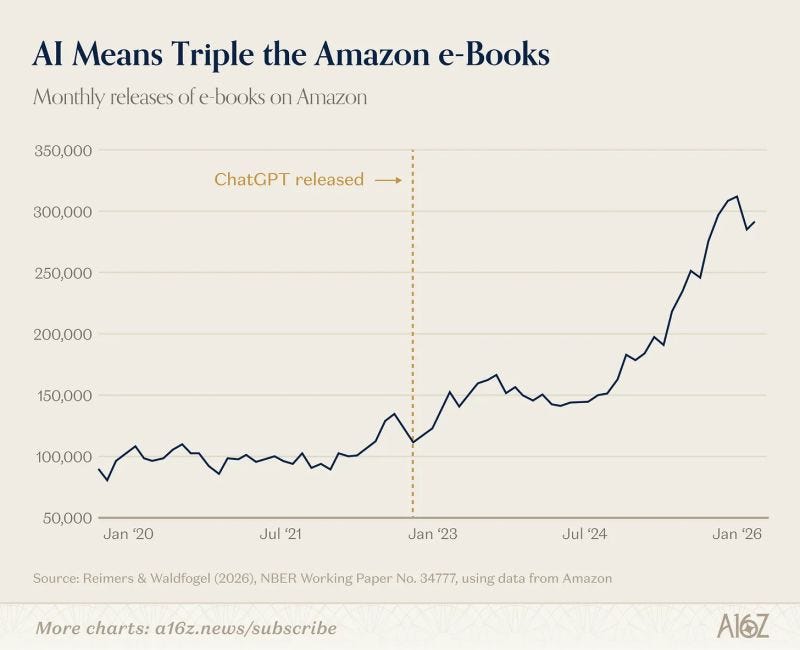

AI Chart Potpourri

As promised, here’s a few interesting charts that came across my desk this week regarding AI.

The first is regarding e-books, which have—as expected—tripled in volume in the past two years. The amount of slop is increasing, and the Kindle store is full of it. I expect this problem to only worsen, and I don’t have a practical solution because AI detectors are so hit or miss.4

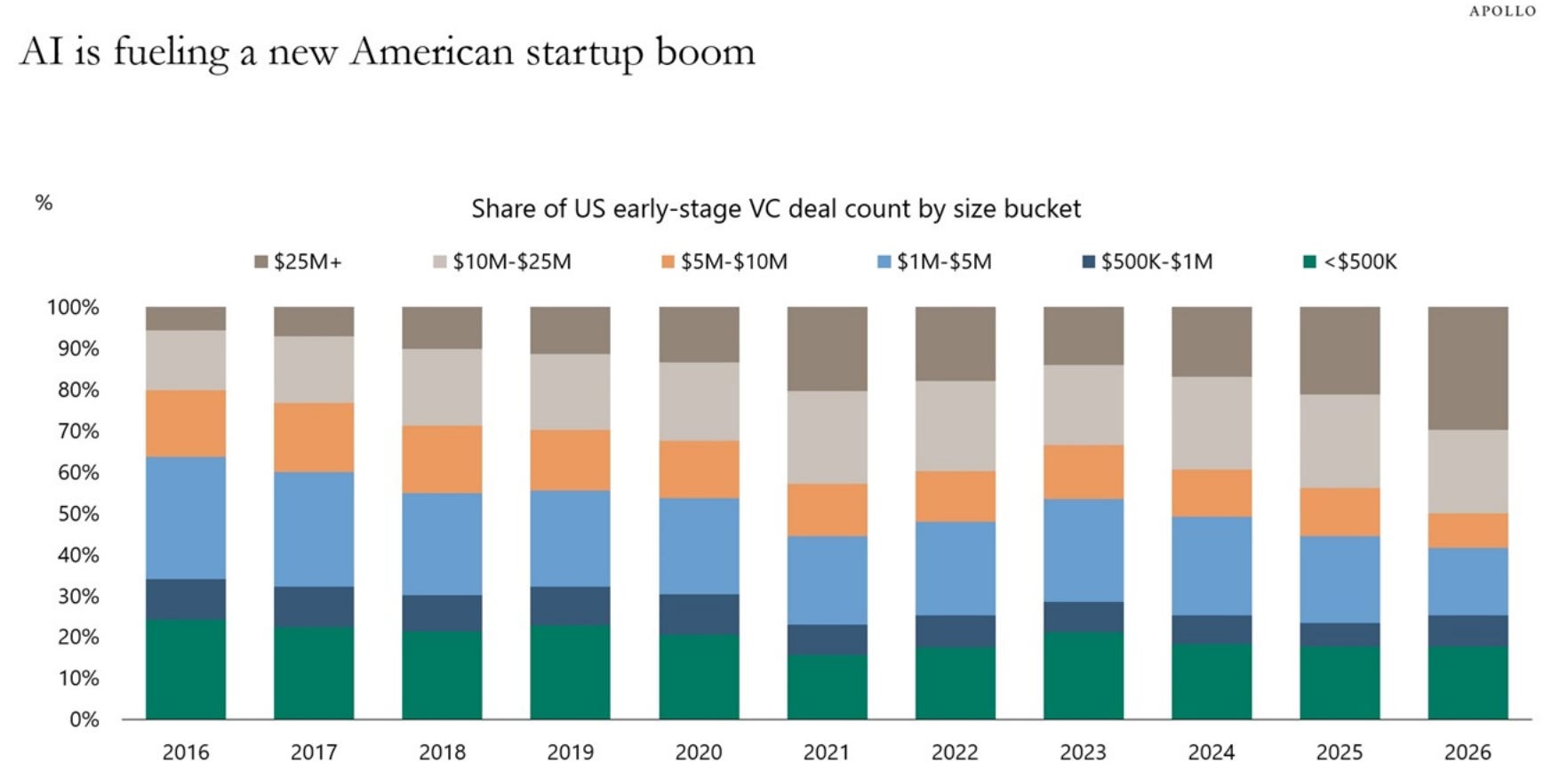

I covered this briefly in “State Your Business” (TMO #35) and “VC Has a Knife to PE” (TMO #42), but one of my theories on AI is that it will enable the little guy in ways that large corporations won’t be able to take advantage of, because oddly enough, I don’t think most generative AI processes save enough money to be worthwhile for large corps.

But a guy in his basement can deal with a little slop in his code. Lo and behold, VC deals are getting larger and larger as startups take share of the market. They can leverage tools others can’t, and it means the floor for what VC will take is now much higher.

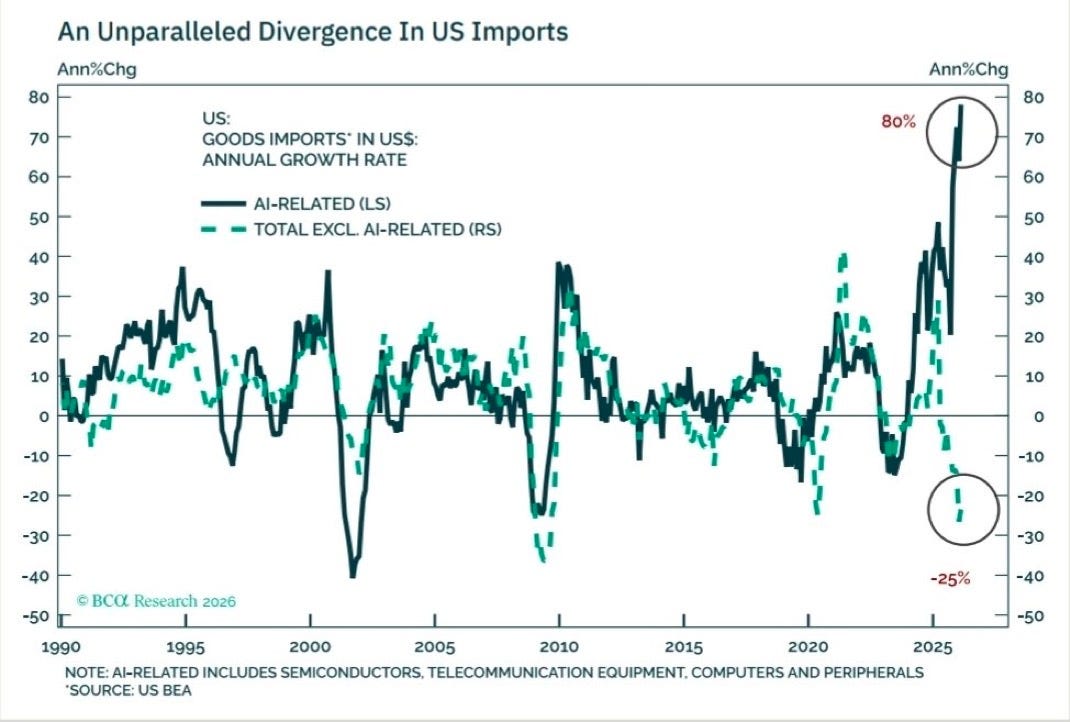

An interesting trend in AI has been imports, something I covered back in “The AI Economy Expands” (TMO #29). AI-related imports are surging, up 80%, while imports of basically everything else are down significantly following the Liberation Day tariff debacle.

I would expect this broader import rate to correct now that tariffs are being dismantled, although it’s still really unclear what the fate of those will be. It seems unlikely to me that Congress will authorize the new rates to stay more permanently, but I could be wrong there.

All of this is very bullish for Taiwan, which is where most of the AI-related imports are coming from.5

We’ll see how much this will affect GDP, but I have a feeling that unseating the consumer as the primary determinate of economic growth will be very, very hard. When you control 70% of GDP, it’s hard to fight you.

We’re not importing so many chips that the math around that has changed…Yet.

If this newsletter made you think of a pal, send it to them and tell them why.

See you next week.

Out-of-court restructuring of a delinquent firm designed to avoid formal bankruptcy.

Plus, markets tend not to reprice the same risk twice. Once it was over worrying about Iran, it was over it. Unless oil shortages start to take place, I doubt the market starts really falling again re: Iran.

Also, when I saw this chart, all I could think of was WWE’s Michael Cole screaming “RKO outta nowhere!” Relevant YouTube link.

I’m writing this from a home in California that was built in the 70s, where my commute to my city’s downtown area where I work (hybrid, mostly remote) is ~8 minutes. But when I was a teacher, I used to commute 90m/day.

I’m grateful for my new working arrangements.

For now, the best solution is still “have taste,” but I understand that’s not practical to say to people.

I recommend curious folks take a look at this video from TLDR News regarding the state of the Taiwan dollar.