The Volatility Express + Portfolio Update

It's getting risky in here, the bots are taking jobs that don't exist, hundos are in style, and the TMO Model Portfolio continues to trounce the S&P 500 by ~8%.

Welcome to this week’s edition of The Macro Obsession.

The best round-up of current events and trends in finance, tech, and the real economy currently in your inbox!

Issue #40—Week of April 6th, 2026

Risky Business

Rocky Job Market, Solid Bot Market

Cashing Out

April TMO Model Portfolio Update

Hey folks,

Happy Passover and Easter! This week, I have two quick announcements.

The first is that I’ve extended the TMO archive timer to four weeks from two. This applies to all issues moving forward, including this one. Happy reading!

The second is that it’s April! And a new month means a TMO Model Portfolio update and a new edition of The ETF Obsession. Get hyped!

If you missed the first one from last month, The ETF Obsession is a monthly publication where I look into every ETF that launched the prior month.

Out of the 62 ETFs launched in March, only 4 were worthwhile.1

You can check out the article here:

Now, let’s get on to the newsletter. Thank you!

Risky Business

As the head of Global Macro at Fidelity, Jurrien Timmer put it, the “jaws of risk are wide open.”

I still think we’re at or past a local bottom in equities; see last week’s “Profits Justify Price” (TMO #39) and this next footnote for more discussion on that.2

We can see it in the chart: stocks are down, stock volatility (“VIX”) is up, bond volatility (“MOVE”) is up, crude oil prices (“WTI”) are up, and currency volatility (“CIVX”) is up. Some are well above, and all are nominally above their 50-day Z-scores.

In plainer English, volatility is elevated across effectively all assets, even cash.3

Meanwhile, private asset managers range from “mildly depressed” to “eating dirt.”

They’ve been under fire since the First Brands and Tricolor bankruptcy woes back in September (Reuters). Jamie Dimon, CEO of JPMorgan, sealed their fate when he said the now infamous line in a JPM 0.00%↑ earnings call:

…When you see one cockroach, there are probably more.

I’m still on the fence about how I feel about private credit. This collapse in asset managers prices seems warranted. But how much further will this go? I think they may rebound when the market does, but likely not back to where they were. There are more holes in the ship than before, but I’m not sure that there will necessarily be some greater blowup.

Despite all the headlines of doom and gloom and the funds that are restricting withdrawals (WSJ), it looks like the market has already taken care of who needs to be punished. Blue Owl OWL 0.00%↑ being down ~45% YTD seems to be an appropriate response to the situation.

Sentiment is in the dumpster. You know it’s bad when large private market commentators like Leyla Kunimoto are cracking these kinds of jokes.4

The market is much more certain about private credit than I am, and it seems to be pricing in calamity. It does make sense, especially because these firms were billed to many investors as private equity firms that dabbled in credit. These credit funds started as a side part of the business. But over the last few years, these entities have changed their core exposure.

What used to be a bet on private equity is now a bet on private credit.

So there’s no “growing our PE portfolio” out of this unless they see a lot more LP money coming in…And right now, that’s the opposite direction of where LP money seems to be going. Time will tell if that trend reverses when rates inevitably are dropped back below 3% long-term, although who knows when that will be at this pace.

And no, I’m not buying the GPZ ETF GPZ 0.00%↑ here to catch a rebound, though I considered it.

If you can think of a clean way to express “long GPs, short LPs,” let me know. That’s the trade I really want to take. The GPZ ETF nails the long part. How does one express the second part? Seriously, let me know.

Rocky Job Market, Solid Bot Market

AI is the cause of many problems, it turns out, including some job woes, though the official TMO line here is that it’s probably overstated, and I worry about young people in particular. I’ve also speculated that it’s the cause of certain pockets of unemployment, like in junior software developers (TMO #35).

This week, we got some great data on what I think is the best articulation of this theory about AI’s effects on the job market yet.

It’s not really about jobs being taken, although layoffs are happening and AI is being blamed by both managers and workers alike. But I doubt the claims that departments are being filled by AI workers. We’re just not there yet for most businesses, even if integration is happening.

No, instead the primary effect will be on how many future jobs we have. I think that AI is killing job potential, not existing jobs.

As Labor Matters (Gad Levanon at the Burning Glass Institute) put it when he released this data:

To gauge the impact of AI on jobs, the real question isn’t whether employment is rising or falling. It’s whether employment is where we’d expect it to be if generative AI had never arrived.

That requires a counterfactual.

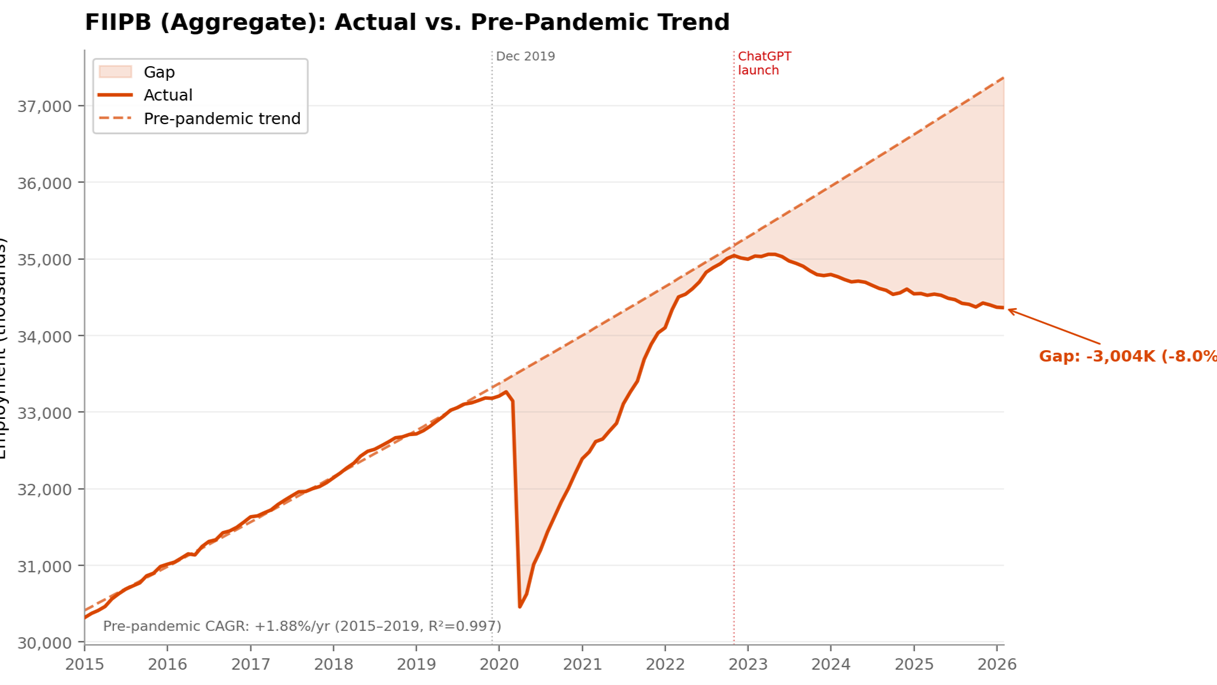

Take the five industries at the heart of the white-collar U.S. economy: Finance, Insurance, Information, Professional Services, and Business Services—what I call FIIPB.

Here’s the FIIPB vs. its old trend. We’re 3,000,000 jobs short of where we should be if the 2015-2020 trend held up. Yikes.

Add 3 million jobs to this current economy (without pulling anyone from outside the labor force), and you cut unemployment down 200 basis points, from 4.3% → ~2.3%.

The largest hit category was information workers, which makes sense since they are the easiest workers to replace with AI. They were also the ones that benefitted from the hiring spree pre-ChatGPT.

If this trend continues, it’s obviously a bad thing for our services-based economy. I suspect that there will be a plateau hit soon. There are only so many people you can get rid of before things start to fall apart on the business level and tasks that cannot be automated without a human “in the loop,” as they say.

We’re already decelerating the potential job losses. The question is where that plateau is. This bleed will last a long time.

Cashing Out

This story was a surprise to me when I saw it, because my mental model of cash is that it’s a dying thing. Of course, in my life as a suburbanite in Southern California, I feel that way. I only ever need cash to pay for tacos on the side of the road.

But most people do carry cash, including myself, even if we try to avoid ever using it.

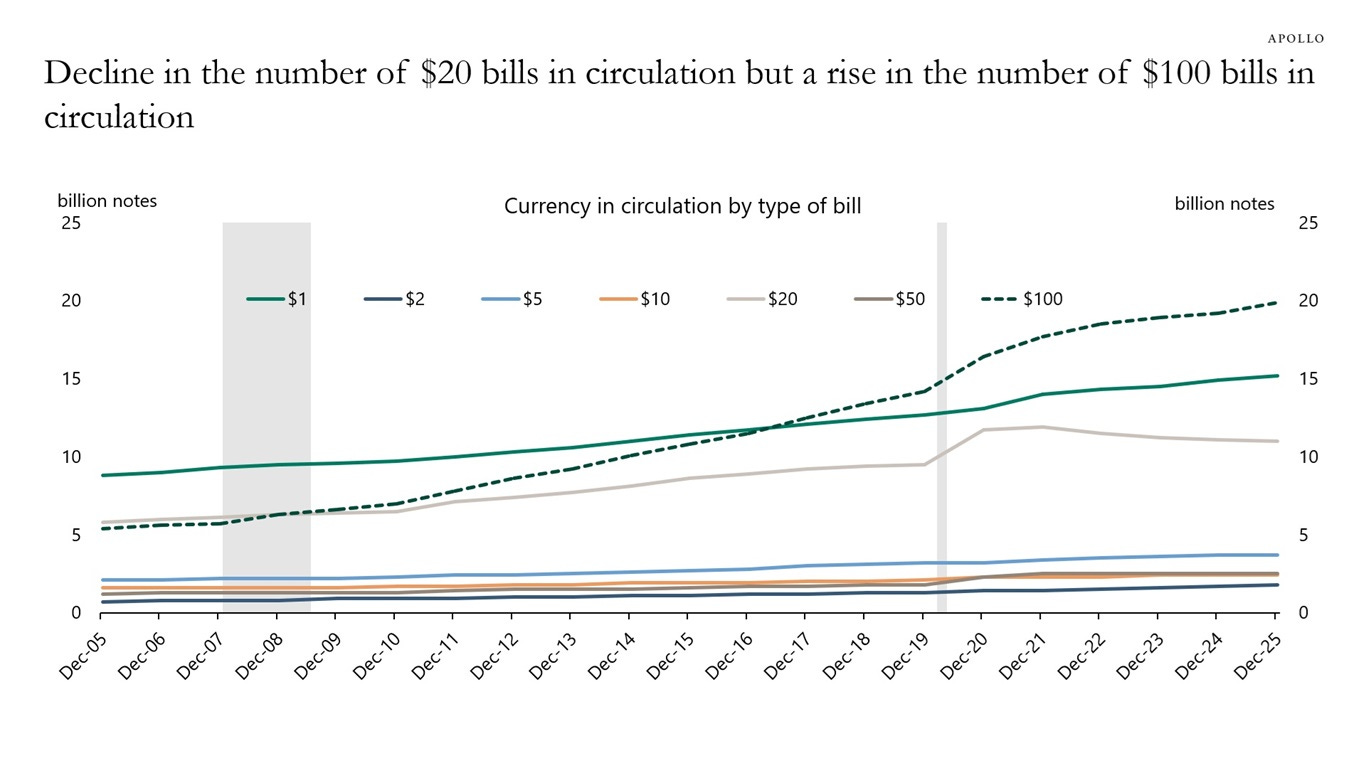

My belief was that cash was largely used for low-value transactions in person, and even that was dying. Physical cash makes up 7% of total transaction value but is still ~35% of transactions <$10.

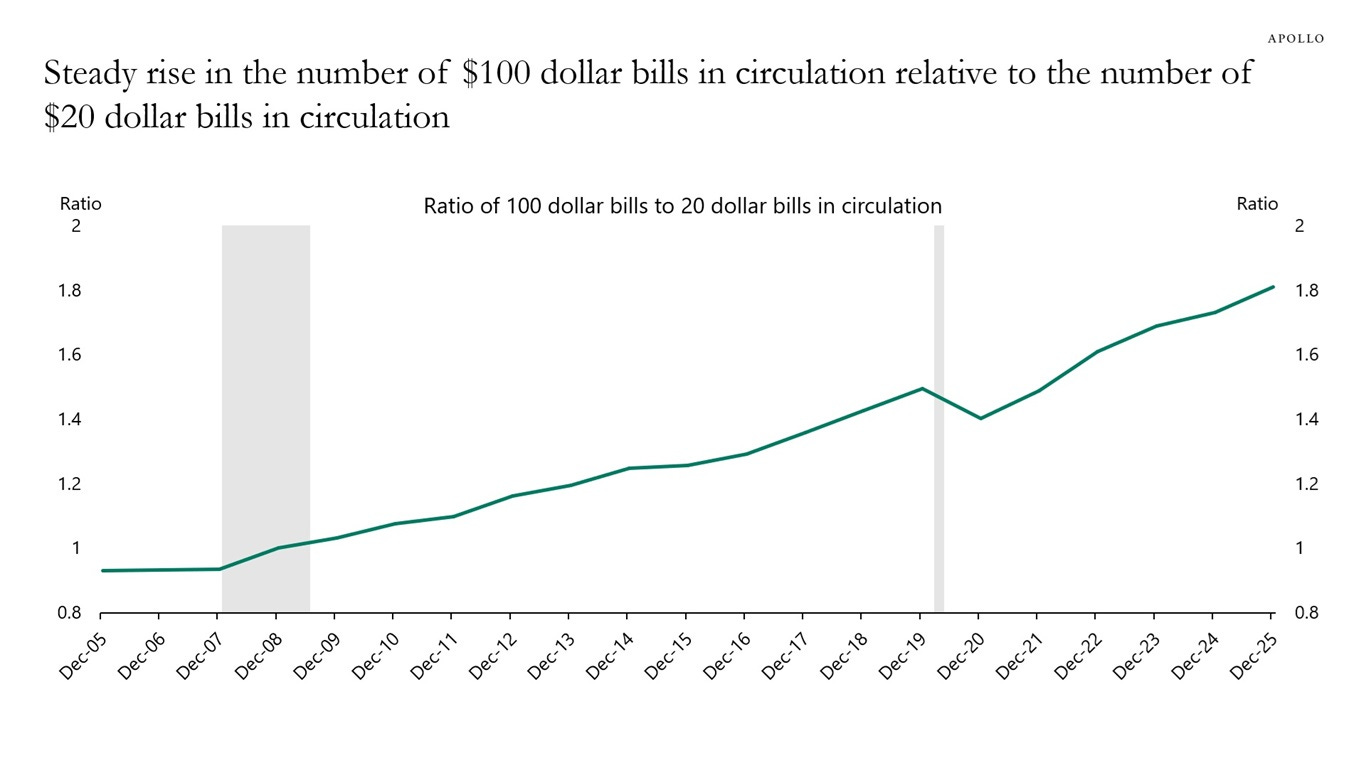

I’ve never seen data on this topic before regarding the number of bills in circulation. $100 bills overtook $20s a long time ago, but I hadn’t realized that the trend accelerated post-2020.

What I would expect to happen post-2020, a decline in the use of bills, did happen to all other denominations, but not to Benjamins.5

But that trend is not abating for $100 bills. Perhaps the cash carriers are all loading up on Benjamins instead of Jacksons now?

Cash may be coming back to some degree. NYC just passed a prohibition on cash bans (NYC.gov) in stores, although I’m pretty sure they can still refuse bills over $20. I am not sure how this will affect all the hundos in circulation.

Who is using all of these big bills, and what are they using them on? Too micro for me, but I’d love to know the answer.

Either way, at the current pace, we’re going to hit a 2:1 ratio in a few years.

More Below, But ICYMI

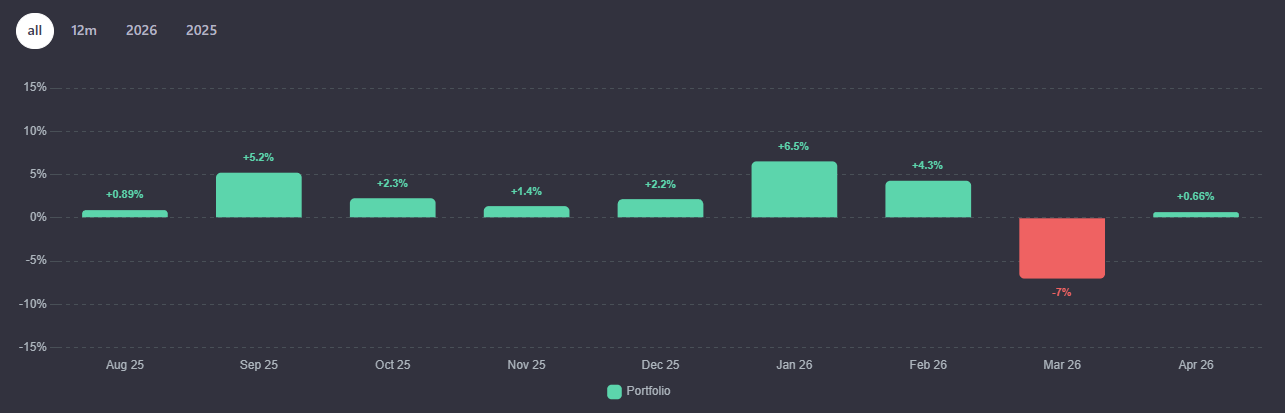

April 2026 TMO Model Portfolio Updates

Every month, I give an update on my model portfolio—the portfolio I’d say to follow along with (and change to fit your style)—if you wanted a low-turnover portfolio that beats your financial advisor’s boring 70/30 or 60/40 portfolio.

It owns 10 ETFs only and makes a trade once every 2 months on average. If you missed it, there was a trade alert on March 22nd where a piece of the rotational strategy was shifted.

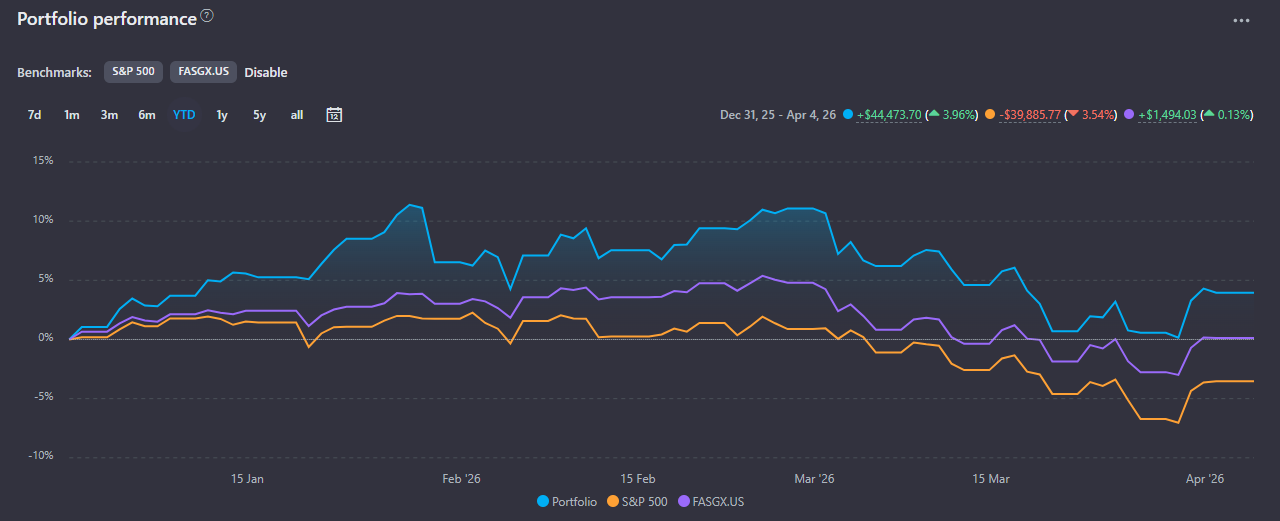

The Model is outperforming both its benchmark and the S&P 500 YTD (and its lifetime), returning 3.96%. 6

March snapped the winning streak and became the first month on record that the portfolio has lost. This was to be expected, but it took a lot longer than I thought to hit a snag. The combination of equities and precious metals selling off in tandem hurts the portfolio strategy big time.

This monthly drawdown was larger than any up-month, although the portfolio still has a positive open PnL on all open positions.

Over its lifetime, since it was launched along with this newsletter in August 2025, The Model has returned nearly ~14% more than the S&P 500 and ~10% higher than the benchmark; that is compounding at work, even on a short timeframe.

Free subscribers, this is where we part, as I keep discussions of the individual assets involved in the portfolio reserved for premium subscribers.

If you’d like to access The Model, here’s a discount link that works for life7:

Thank you, and I’ll see you next week.

Premium subscribers, welcome beyond the paywall, and thank you for your support.

Use the link below to track the TMO Model Portfolio, see all of its transactions (low turnover, not too much to see, but it’s all there), and its live holdings: