Strait and Narrow

Oil has a 1 in 7 million day, I consider shorting Euroairlines, the S&P 500 hits the line in the sand, the Great Retirement's tail is flattening, and I promise this is the last strait crack.

Welcome to this week’s edition of The Macro Obsession.

The best round-up of current events and trends in finance, tech, and the real economy currently in your inbox!

Issue #37—Week of March 16th, 2026

Six Sigma Spring

Auf Wiedersehen, Lufthansa!

The Rotation Bottoms

Grandad’s Back At Work

Hey folks,

Earlier this week, I released the first edition of my new monthly publication, The ETF Obsession. It now has its own tab on TMO's homepage where it and future editions will live.

I researched every exchange-traded fund that launched in February. There were 89 fund launches, but only 12 of them were worth considering.

At the end of the article, there is a searchable and sortable spreadsheet with all the funds, their details, and my notes. And if you’re an AV person, I made a YouTube video for you.

The ETF Obsession | February 2026

Most of the funds launched in February were not worth the time I spent on them, so please let me help you avoid spending any time you don’t need to researching newly launched ETFs.

Okay, onto the newsletter!

Six Sigma Spring

Traders have been getting whipsawed on oil, as the fate of the Strait of Hormuz remains unclear. It’s been a week since I wrote this in “Safe Haven No More (Revisited)” (TMO #36):

As long as there are reports of missiles being fired out of Iran, we cannot say that the strait is open.

It’s not about who says the strait is open or closed. Trump or the IRGC can rattle their sabers all they want and offer whatever deals they can think of, but the tape doesn’t lie.

All that matters is that tankers are willing to cross the strait.

Currently, they are not.

That unfortunately holds this week.

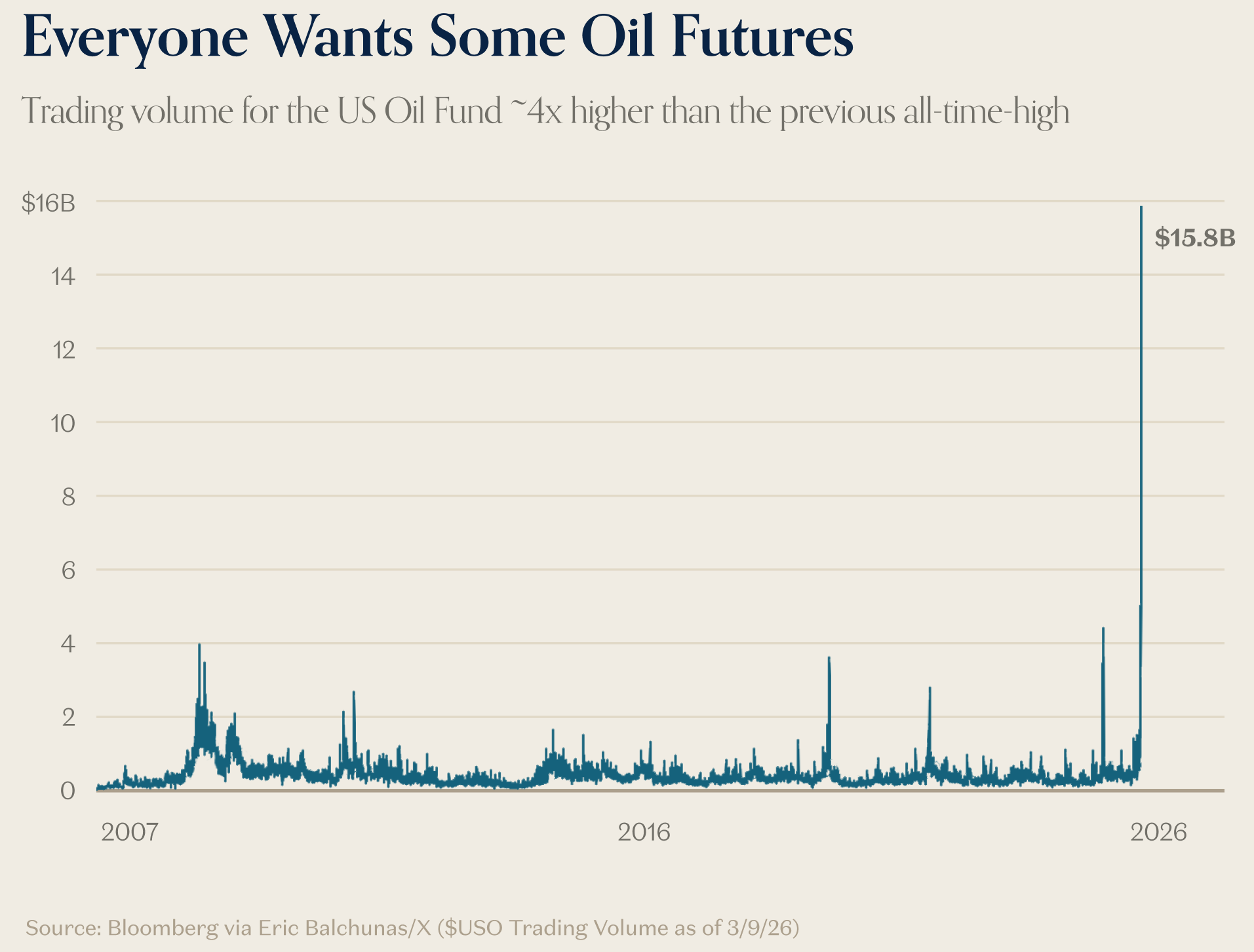

Beware of chasing oil at this current moment. Unless you have your nose to the news, this trade is radioactive. I think we can safely consider it “crowded.” Trading volume for the US Oil Fund USO 0.00%↑ hit more than triple 2020’s previous records.

For those curious, all that volume resulted in a net inflow of $984M (ETF.com). The bias is about 6.53% positive, so that should be somewhat comforting for the bulls.

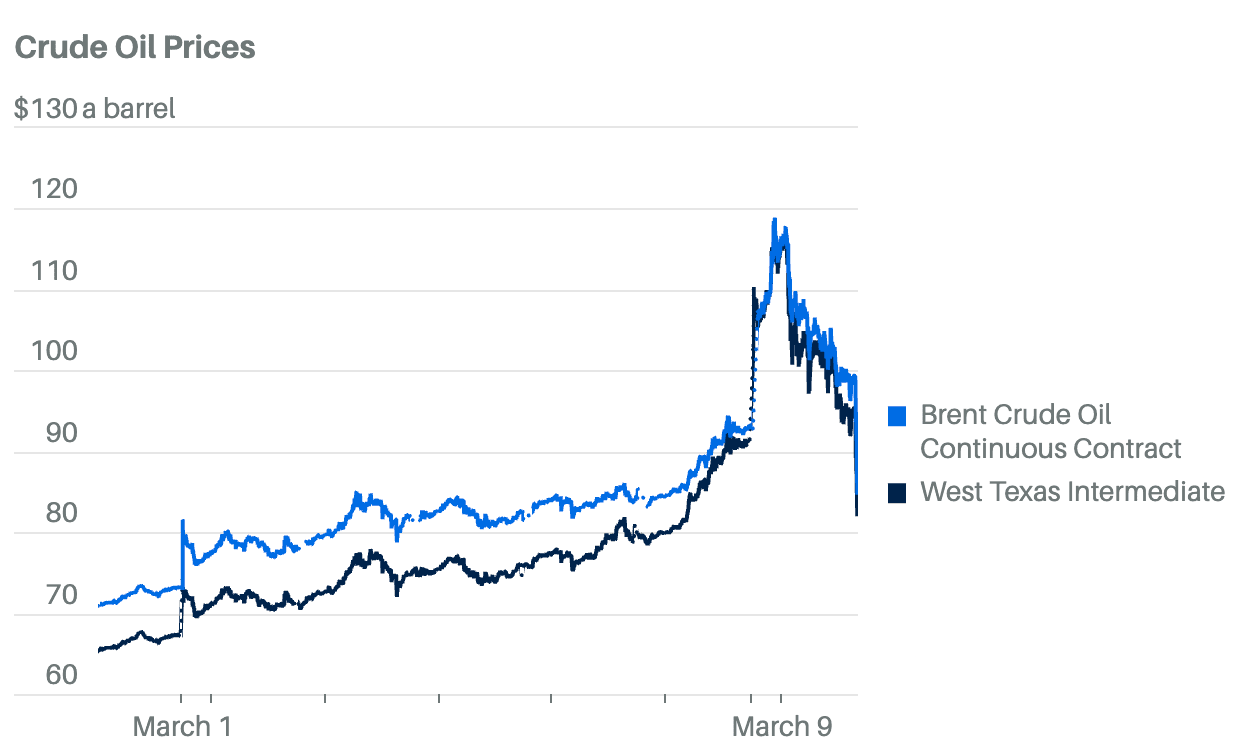

Beware, one has to be willing to take some pain if they’re wrong with a trade like this. Consider the sheer amount of money both made and lost during the March 9th rollercoaster from $91 at last close → $120 intraday peak → $82 by end of day.

The nerds in my audience will appreciate that this was a six sigma event (Quantra), or a 1 in 7 million occurrence.1

There were some positions in oil that are still underwater despite the war arguably getting hotter since then.

I won’t be able to say when, which is what really matters, but I can safely say that if we get news of peace and mutual de-escalation, it will likely be sudden. It will also take oil straight down with it. Don’t get caught in harm’s way.

There is also the possibility that I’m wrong. Degenerate crypto betting markets think there’s a ~40% chance we invade by December.2

That would absolutely give us oil above $120, and one would be very validated buying oil at the current levels.

I would honestly start to consider the bearish $200 scenarios at that point—very, very bad for the real economy that very much runs on oil.

To cap this story off, here’s a much lighter alternative solution to the whole thing that came up on my feed this week and was too good not to share:

Auf Wiedersehen, Lufthansa!

One of the stories that caught my eye this week was that European airlines (“Euroairlines”) have been hit in a double bind that made the STOXX Airlines index (STOXX) tumble 15% over the last two weeks. I figured airlines in general would be hit, but Euroairlines have it especially bad.

The first issue with the airlines stocks is that the rise in oil prices has spiked jet fuel. That is what fueled this first leg down in the index. It’s an easy headline for traders to sell on: input costs go up at no fault of the firms.

In hindsight, this should’ve been an easy short when I first heard that the USS Gerald R. Ford was heading to the Persian Gulf (Reuters) a month ago.

The reason I say first and not only is that I believe we could easily see a second leg down for Euroairlines if this conflict drags on. There’s an issue that I haven’t seen the media talking about enough, which is that these airlines have been having to reroute around Iranian airspace due to its closure.

Add in the closure of both Russian and Ukrainian airspaces that were already in effect, and you’ve got all Euroflights to Asia booked through one little corridor over Azerbaijan.

Not only is that definitely within Iran’s striking range,3 but Azerbaijan is in the middle of a peace accord process with its neighbor Armenia over a long-contested place called Artsakh or Ngorno-Karabach, depending on which side you’re on.

Central to this peace deal is not only the U.S. but President Trump himself and the TRIPP deal (Geopolitical Monitor). The long and short of it is that the agreement is tenuous, holding off a small war that could close Azeri airspace—not because the Azeris will close it or the Armenians will force it closed, but because the Euroairlines will make moral objections, like they do with Russian airspace—and is overtly counter to Ruski interests in the region.

If there were a time for the Russian lobby in Armenian politics to pull a lever and tank the deal, this would be it. Making chaos on Iran’s border that takes American attention off Iran itself is a good thing for both Iran and Russia.

Notably, the deal favors the Azeris, so I would expect any issues with it to come from the Armenian side.4

A Quick Peek Into The Lab…

Here are the stocks I’m watching for this trade, but I would only put this on if I saw something credible coming out of independent media:

Air France-KLM — $AFLYY

Lufthansa — $DLAKY

AIG — $ICAGY

Ryanair RYAAY 0.00%↑ may be tempting because it trades as a Nasdaq ADR instead of OTC, so access might be better for my readers. But they don’t have major Asian flight exposure, so they're not a suitable candidate for this thesis.

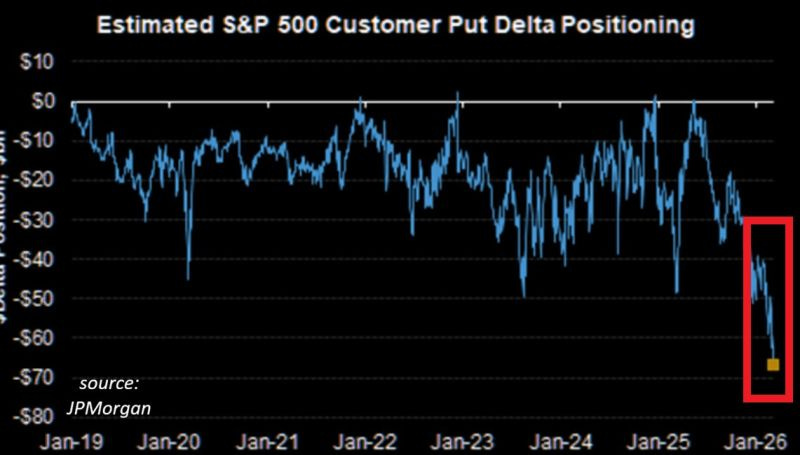

The Rotation Bottoms

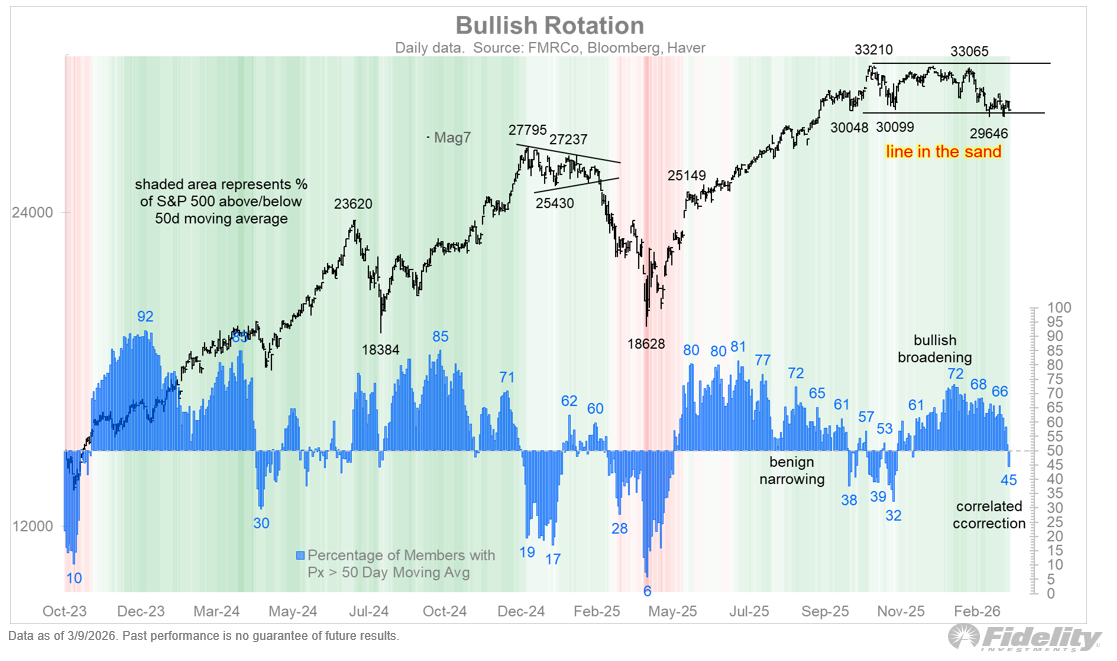

The ongoing bullishness in small caps and value stocks that we’ve been covering since “Revenge of the Small Caps” (TMO #24) has hit a new level, what the head of global macro at Fidelity calls the “line in the sand.”

I’m still not a buyer of the rotation here, quite the opposite. I am happy for TMO’s Model Portfolio to be overweight U.S. megacaps in its current allocation.

It may feel dangerous at times to do nothing—we didn’t make any trades this month, waiting to decide until the April update on the rotational strategy, but otherwise, we’re just holding on.

Meanwhile, I keep getting blasted with data showing traders pricing in the apocalypse. This kind of extreme hedging makes me nervous, but I understand that after a few years of killer stock market gains, folks have a lot more to protect than they did back then.

Historically, this kind of positioning usually indicates a bottom.

And for those that fear war, remember that markets are forward-looking, humans have a bias toward optimism in action (not always in thought), and that there is a long-standing precedent of markets surviving things like this.

More Below, But ICYMI

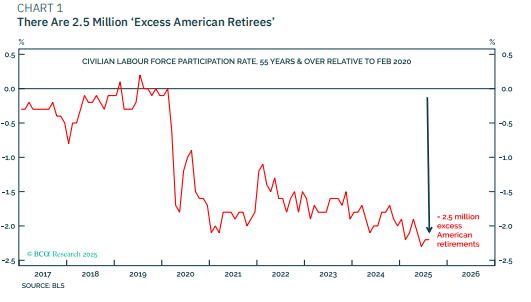

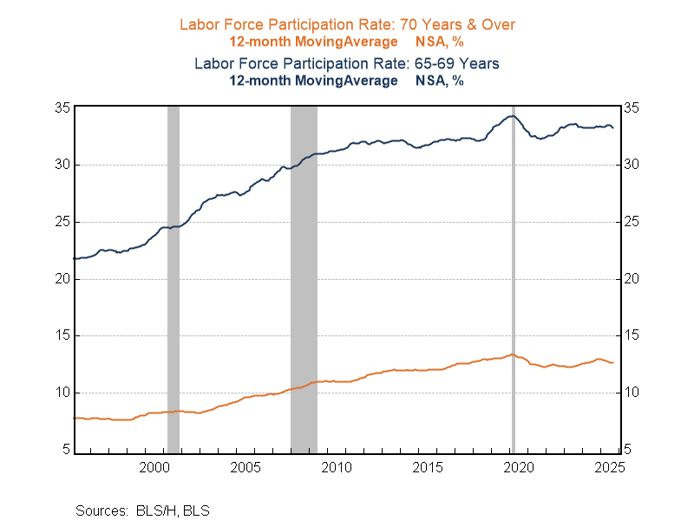

Grandad's Back At Work

I love a good update to an ongoing long-term thesis, so let’s conclude this week’s round-up by partially answering a question that I posed a few editions ago: “How Long Will The Great Retirement Last?” (TMO #22).

The gist is that we’ve seen a decline in labor force participation in over-55s since 2020 that has amounted to an excess of 2.5 million people leaving compared to the pre-pandemic trend.

New data on over-65s is showing us a flattening out of their retirement curves, with an uptick back toward pre-pandemic trends last year that is especially pronounced in over-70s.

Turns out, the answer is it’s ending for the oldest workers. I am not sure why this has changed, besides some mean reversion of new over-70s working at the same rate as they used to before the pandemic.

Importantly, we’re not seeing this trend with the over-55s, who are staying retired. The tail of the Great Retirement is flattening, but I’m not sure why. More data is needed.

If this newsletter gave you a new perspective, send it to a pal.

See you next week.

For some perspective, if we observed 19,000 years day-by-day, this kind of event happens on a single day.

Remember from “Jesus Futures Pay 7%” (TMO #30) that these markets rely on a “source of truth” mechanism. This means that there could be disagreements with a particular resolution, and it comes down to a third party—sometimes very vaguely established as “consensus of credible sources”—to settle them. These sources of truth often have no connection to the market, purposefully, but it means that the accepted narrative that settles the market could be fraught with human reporting flaws.

To be clear, this is not me predicting some kind of event with Iran targeting civilian airlines; I would not put that juju into the world.

I’m just saying that the U.S. and Israel killed the current Supreme Leader’s family, including his father, wife, sister, and several of his nieces and nephews. He was then personally wounded and described by Secretary Hegseth as “likely disfigured.”

There’s a passage in The Art of War that explains why cornering your enemies is a poor thing to do. They will act desperately. They will play dirty. They will try to hurt you just as badly as you hurt them. It's always better to let them have a diplomatic out to the situation. They are far more likely to take it.

After speaking to a friend who is plugged into the Armenian diaspora and is a TMO paid subscriber (because he knows what’s up), here are the sources I’d consider following for those who want to be nose-to-news:

https://zartonkmedia.com/

https://www.thearmenianreport.com/

As always, consider your source and their bias with reporting, but if these stray from the state narratives about progress on the deal, that’s the signal.