Bloody Friday

We endured a 7-hour sell-a-thon, plus I talk about the labor market, advanced manufacturing, and bond fund performance.

Welcome to this week’s edition of The Macro Obsession.

The best round-up of current events and trends in finance, tech, and the real economy currently in your inbox!

Issue #49—Week of June 8th, 2026

Risk Off, Everywhere, All At Once

Chip Fab Killed the Toaster Plant

Grandad’s a Job Hopper

Honey, I Fired the Portfolio Manager

Hey folks!

Just a heads up, as of today, I’m out traveling.

This week, I’m leaving my little duplex in Southern California to visit my family out in Northern Virginia. It’s always fun going back to where I grew up, right in Data Center Alley—or my favorite way I’ve seen it put, Colocation Mecca.

My wife1 and I will be spending time with my sisters and my nieces and nephews, getting used to using the right naming conventions for freeways (“No, Jack. It’s not The 95, it’s I-95, or just 95.”), and visiting museums. I miss living near the Smithsonian complex in DC so much; the current plan is to make stops at both the American and Natural History Museums, but we’ll see what we get up to.

Most importantly, we’ll be getting a break from the speed in which we live our lives on the west coast. I’m dead serious. Living in the Los Angeles metro area has made my gait faster. When I travel anywhere, I realize just how much I speedwalk. It’s just the default outdoor walking speed in SoCal.

So if you message me, comment, etc., and I don’t get back to you, that’s why.

Alright, onto the newsletter!

Risk Off, Everywhere, All At Once

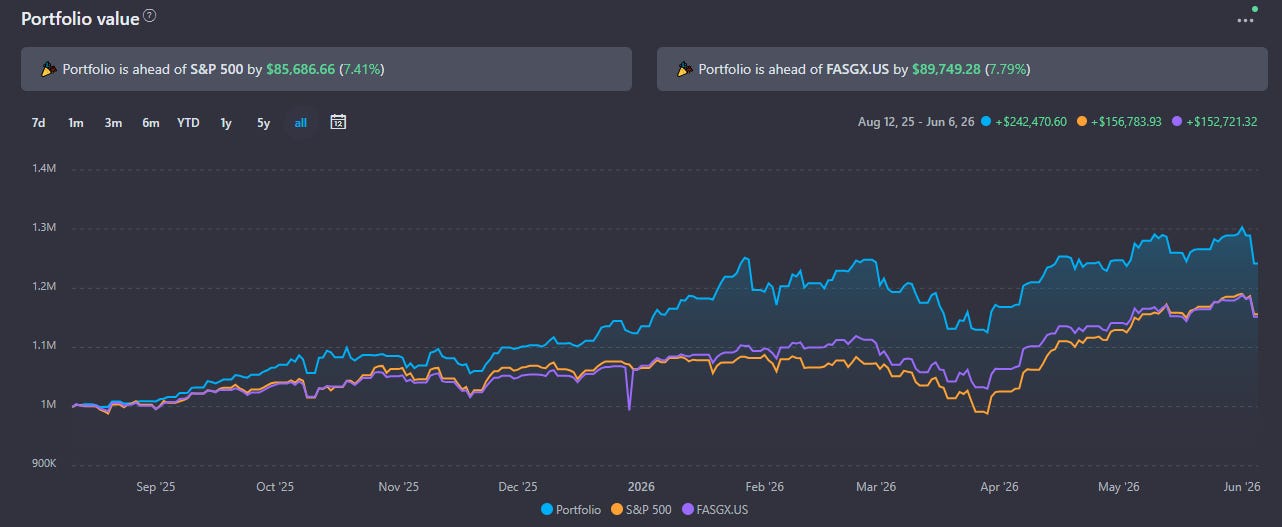

Friday was a doozy of a day in the markets, although I know I don’t have to tell readers of this newsletter that. But I just can’t help myself when we get the largest single-day selloff in the Nasdaq since Liberation Day at the end of the week that I posted “Feeling Bear-ish + Portfolio Updates” (TMO #48).

I’m glad we made those changes to the portfolio when we did.2

Here’s the Nasdaq from the past five days. Friday is framed, and there’s a line at the top of the lowest hourly volume bar, so you can see how relatively elevated it was.

It wasn’t just the Nasdaq 100; precious metals, base metals, treasuries across the curve, crude oil, and basically everything apart from the dollar puked. There were very few assets one could be hiding in to avoid that pain, and cash is the only one worth holding through any of the good times.

Bonds didn’t save our portfolio’s 70/30 benchmark, and I’m still glad the portfolio has dynamic duration exposure. Nothing but being short or sitting in cash would’ve been the right move. At least we don’t own any crypto; it’s getting slaughtered compared to everything else.

A brief update on the portfolio’s performance because holy wow—that drop in stocks and metals at the same time hurt. But I’m not worried; in the grand scheme, we’re just back at levels from a few weeks ago. Nothing about my conviction is broken by these price movements, so no need for any updates on that front.

By the way, I was serious when I said that was the last time I was going to offer 20% off TMO subscriptions. So go check out last week’s issue if you want to read more about the portfolio and decide if you want in before that code gets disabled at the end of the month.3

Back to the task at hand, the jobs report:

Ultimately, the culprit was that the jobs report from the BLS gave the market hope for a rate hike. Long story short, this sell-off was an overreaction. It may carry on for some time, but that’s part of investing.

Asset prices don’t just go up all the time. This is one of the times when I’m happy about my personal timing with the early take profit and minor rotation, but otherwise, I’m sitting tight and staying long.

If you want to read my commentary about the report itself, take a look at the article I wrote for Seeking Alpha [GIFT LINK] and the commentary I gave for Charting the Rubicon’s monthly coverage of the data, linked below.

Think TMO is neat? Send it to a buddy!

Chip Fab Killed the Toaster Plant

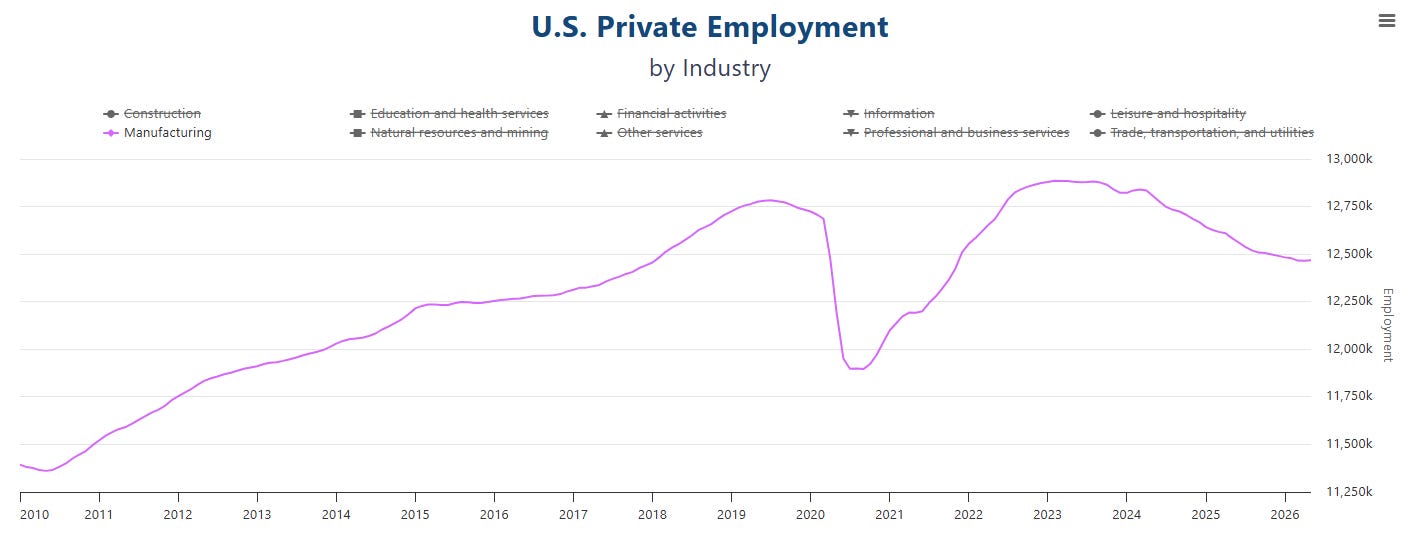

The current administration in Washington’s push for reindustrialization is well underway now, and we’re starting to see the effects on manufacturing, one of their core interests.

I’ve been bemoaning in my jobs report commentary in my Seeking Alpha column for some time that manufacturing employment is not only falling but accelerating.

So if we’re reindustrializing, it’s not bringing jobs with it—at best. At worst, we’re still actively deindustrializing despite all the executive orders and dealmaking that the administration has dubbed “The Trump Effect” (whitehouse.gov).

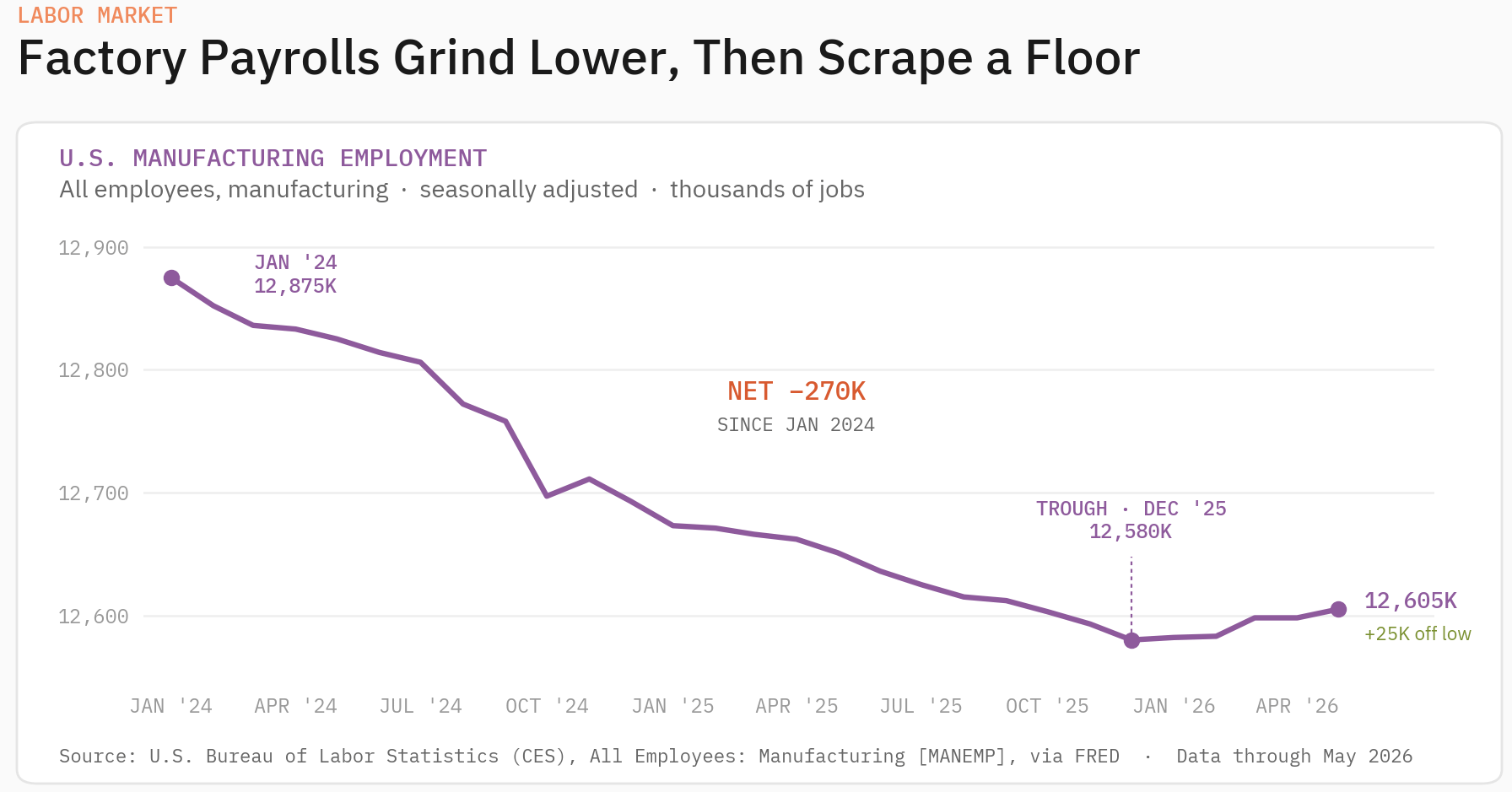

Zoom in on the BLS reports for manufacturing over the last two years, and it’s looking about as bleak, but with a little inflection that’s lost in the wider shot. Maybe December really was the bottom. I find that doubtful.

My central theory has been, and remains, that the manufacturing that’s coming back is largely automatable manufacturing that brings very few jobs. It’s not the kind of manufacturing that went to China decades ago. It’s the kind of manufacturing that the Chinese are trying to move into now that we can still compete with. But we will never be able to compete on labor costs.

The “toaster plant” is never coming back. It had a decent run for a second post-COVID because of the interest rate relief and government welfare (PPP loans, etc.), but fell off again as the current administration came into power.

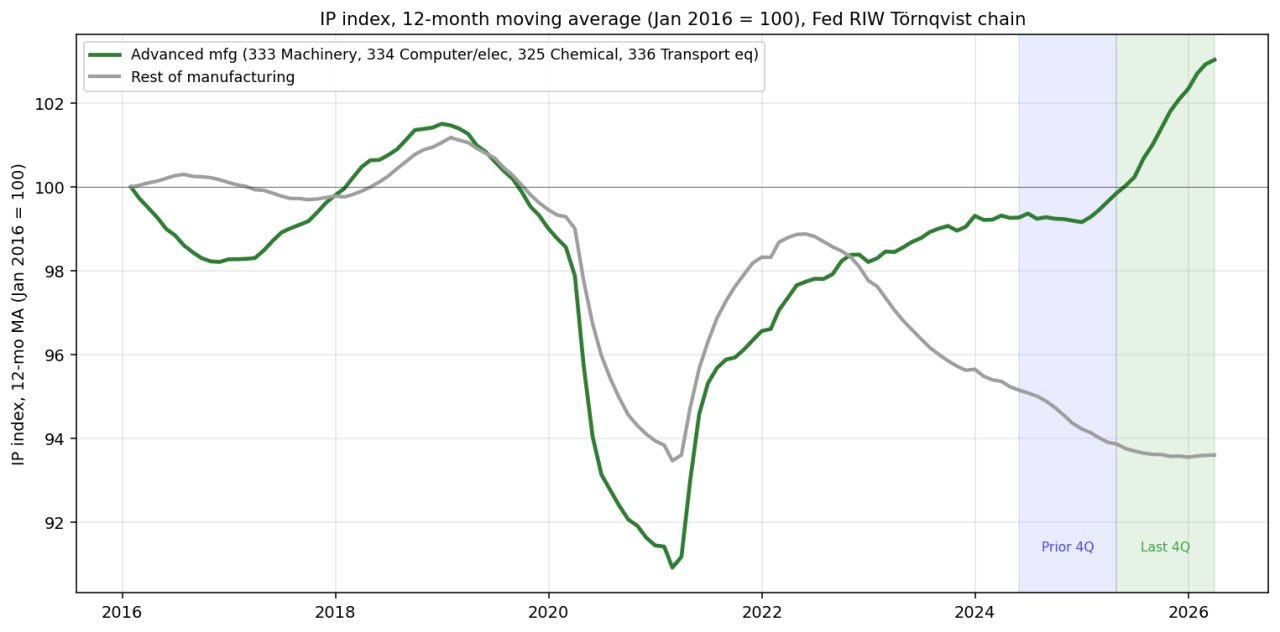

The plants that make advanced machinery, industrial chemicals, jet turbines, and, of course—computer chips—are doing much better by comparison. It’s now higher than its pre-COVID levels, which surprised me to see. The divergence has been ongoing since late 2022 and has become undeniably stark.

Advanced manufacturing actually is coming back. The question is whether it will be sustainable without government intervention and support. Between the government taking equity stakes in corporations, hiking tariffs to previously unseen levels in the modern era, and the president making backroom deals with CEOs, I don’t know how this would be sustained otherwise.

The next administration could kill this trend, for better or worse. The current one might not be able to sustain it. They’re fighting economic gravity. Advanced manufacturing may be the way out of the deindustrialization mess, but if it is, we shouldn’t expect it to be bringing back a lot of jobs.

Grandad’s a Job Hopper

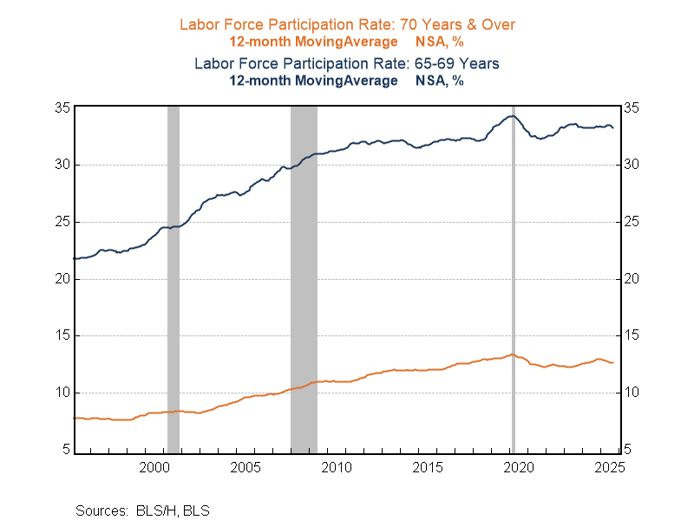

While we’re talking about labor and the real economy, I wanted to give an update on new data I found related to “Grandad’s Back At Work” (TMO #37).

In that story, I discussed how we were starting to see a flattening in the retirement tail; over-55s who retired early have stayed that way, buoyed by asset prices, which was likely also the reason they could retire early. Meanwhile, over-65s who retired on time are—you guessed it—going back to work.

My stepdad retired last week after putting in 37 years at his company. Those years of service are something he’s rightfully proud of, and something that we commiserated is no longer the experience of people in my generation. He’s the last generation that worked there to get a pension that honors his years of service—everyone younger gets a 401(k) match.

Going to his retirement party made me think about this statistic; I’d never considered what could drive him to go back to work. And if he did go back, could he go back to the gig he retired from? Would he find other work? Surely, the benefits wouldn’t be similar to what he had before, and the government provisions can be lackluster at times.

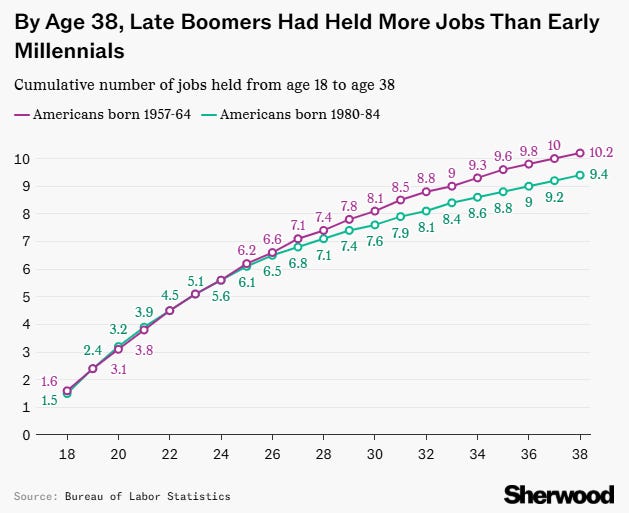

Then, I caught something interesting and worth sharing. Perhaps our view of the worker who put in his time is based mostly on anecdotes, on stories like my stepdad’s. The change we’re noticing may not be a real change in the average worker experience, but a change in the outlier experiences that we find admirable.

Perhaps it’s not that all the Boomers had jobs they worked forever; it’s that the few who did—their jobs don’t exist anymore, at least not in the same capacity that incentivizes sticking around.

When we look at the number of jobs Boomers had vs. Millennials, we see who the real job hopper is. Turns out, the younger cohort moved jobs less through their prime job-changing period.

This data is counting company-to-company moves, not internal job title changes. Perhaps that’s the difference? I’d be very curious.

I’m also going to be looking forward to us getting the data on my cohort since I’m younger than the groups shown above. Anecdotally, I’ve had 9 jobs at 30, so I’m right on the money for the average Boomer experience.

Not sure if I’m really representative—I’m guessing not. Neither is my wife. She’s at 5!

More Below, But ICYMI

Honey, I Fired the Portfolio Manager

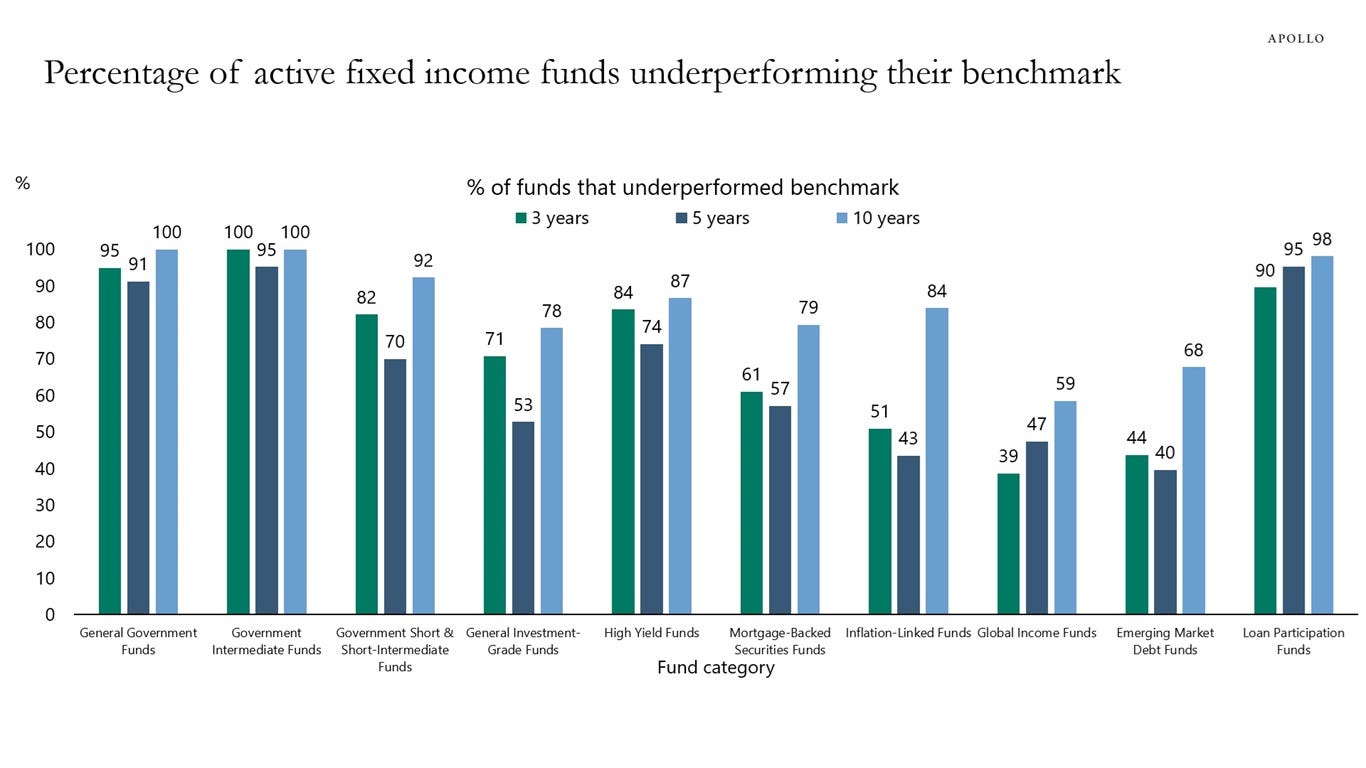

This one is quick because it highlights one of the things that I’ve been saying to people for a while: now is the time to buy individual Treasuries to your preferred time horizon, and I’ve never felt that way before.

Over my investing career, bonds have had yields that were far too low to consider. Yes, they were higher than inflation when sub-1%, but until we started to hit 5%, there were just always more attractive options.

Case in point: when looking at actively managed treasury funds over the last 10 years, they have a 92-100% failure rate against their benchmark.

There was nothing you could’ve done to manage a bond portfolio to save yourself from having bought bonds during ZIRP and then continued to own them through today.

And I’m still not putting bonds into my portfolio, at least not for me in the accumulation phase. I much prefer other assets as a hedge against poor stock returns.

But if you’re thinking that you’re about to retire and a 5% 20-year bond would pay the right amount for you to live and thrive, you might not care as much if it hits 5.5% or 6% later. Something to think about.

See you next week.

Thanks for reading.

For newcomers, my lovely wife is editor-in-chief here at TMO. She checks every issue before it hits your inbox and is often the only force that stands between me and publishing pure, unhinged nonsense. I appreciate her dearly, and I’m not just saying that because I know she checks all my footnotes.

ICYMI, I mandated a trimming of the portfolio’s tech position because of the data I collected in the headline story of that issue (which is free to read), plus I made some other changes that live behind the paywall that made the portfolio more defensive.

I intend to honor it up until the release of the next portfolio update on the first Sunday of July, the 5th.