The Macro Obsession Model Portfolio — October 2025

The Macro Obsession #14 — Week of 10/6/25

Welcome to this week’s edition of The Macro Obsession.

Going forward, the first edition of TMO each month will be a portfolio update, just to simplify the process of tracking that for the paying subscribers. That means that these posts will be paywalled (sorry!), so if you’re here for charts and economics insights and don’t have the $10 to get the model portfolio that beats (and likely will continue to beat) the old 60/40 and 70/30, check out these articles, and I’ll see you next week.

ICYMI:

The AI Productivity Mirage

It’s not all bad, though, since AI is going to make us all more productive… Right?

This is the central promise that AI is supposed to be delivering on: it will change the way we work because it is able to replace so much of the intellectual work that we do.

What’s given me pause lately is the amount of evidence that AI isn’t actually making businesses or people more profitable or efficient. There was the 95% failure rate MIT found with AI pilots across 300 enterprise deployments in the last year. Harvard Business Review found that productivity fell with AI usage at work.

They give a very interesting, and believable, explanation that I think is worth reading in their words.

The Fed is Resisting

The prize at the end of the long war, if Trump can wrest control of the Fed away from the establishment culture, is yield curve control. The Fed has been doing a poor job of controlling the long end of the curve, because the establishment Fed doesn’t believe that it’s their problem.

Powell directly said so at the press conference this week, when asked about the Fed’s “third mandate,” or moderating long term treasury rates, he dismissed it quickly. The establishment Fed belief is that if inflation and unemployment are in check, and are in check long term, then long term rates will follow.

Here is the benchmark from around this time for a few years across the yield curve for US Treasuries (Time to Maturity vs. Yield).

You can see that as the Fed Funds Rate fell, from 5.25% in 2023 (green), to 4.75% in 2024 (red), then to 4% in 2025 (blue), the long end of the curve rose.

The 30yr treasury is higher today than it was two years ago, despite rates having fallen a full 125bp.

The Macro Obsession Model Portfolio

If you missed the re-introduction of my model portfolio, I’ve got you covered. This article goes over the mechanics of the portfolio and its premise.

This article will make the assumption that you have already read this one in advance.

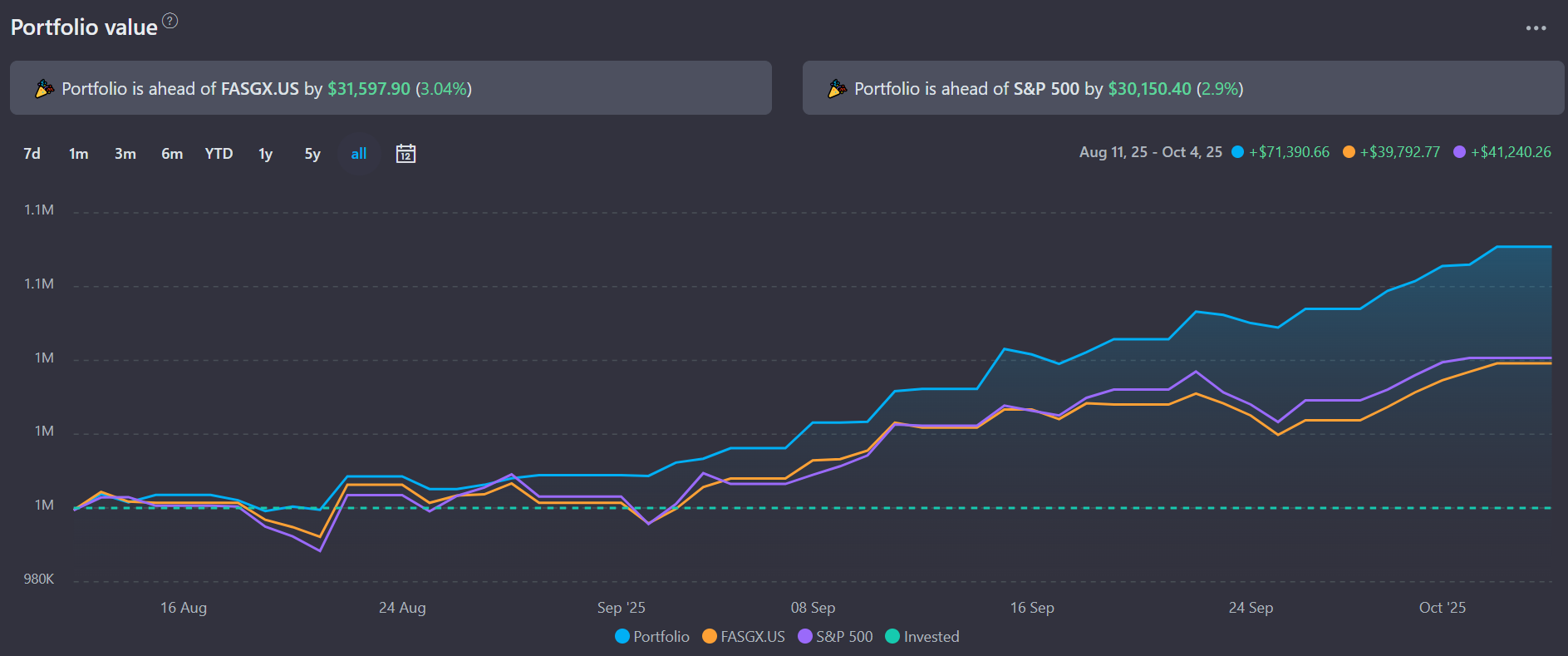

October 2025 Update

I like to be upfront with these things, so let’s just start with the performance. Reminder that this portfolio’s goal is to outperform a 60/40 portfolio of US stocks and bonds, and is benchmarked against a 70/30 portfolio.

I use the mutual fund FASGX to represent that 70/30 portfolio.

Since the launch of the portfolio on August 11th, 2025, the TMO Model Portfolio has returned 7.1%, outperforming both the S&P 500 and the benchmark.